Houston Updates

-

Archive

- June 2025

- March 2025

- December 10, 2024

- September 14, 2024

- May 21, 2024

- March 19, 2024

- December 9, 2023

- June 16, 2023

- April 6, 2023

- March 17, 2023

- Dec. 19, 2022

- Sept. 14, 2022

- July 4, 2022

- March 27, 2022

- March 9, 2022

- September 2021

- April 2021

- March 2021

- September 2020

- August 2020

- June 2020

- April 2020

- March 2020

- January 2020

- December 2018

- June 2018

- March 2018

- February 2018

- January 2018

- September 2017

- September 2017 Post-Hurricane

- June 2017

- March 2017

- January 2017

- September 2016

- March 2016

- December 2015

- September 2015

- June 2015

- March 2015

- December 2014

- June 2014

- March 2014

- November 2013

- September 2013

The U.S. and Houston Finally Returning to Post-COVID Normality: But Where Does the Economy Go From Here?

December 9, 2023

Houston has, for decades, been a fast-growing but volatile economy. Measured since 1990, Houston employment has grown at annual rates near 2.0 percent, although it has slowed in recent years and measured from 2000 to the present has grown at a rate of 1.7 percent. Both rates far outstrip the US economic performance. But Houston’s economy has also been volatile, experiencing seven economic downturns since 1990. Four of these were shared with US recessions (1990-91, 2000-01, the Great Recession of 2008-09, and COVID in 2020), and at least three others were Houston-specific with strong ties to oil markets (the Asian Financial Crisis in 1997-98, the Second Gulf War in 2003, and the Fracking Bust in 2025-16).

Out of all of these downturns the most perplexing for the economist has been COVID. The COVID virus was an immediate shock followed by a massive and immediate public health intervention. Then good fiscal policy was followed by bad policy and far too much fiscal stimulus, and bad monetary policy fed an inflation outbreak that was quickly followed by better policy with rapidly rising interest-rate. Just a few months after the lockdowns ended, a huge financial boom arrived, household income and balance sheets soared, and consumers built up huge stores of liquid assets that kept them spending at high levels long after COVID stimulus money ended. And for much of the last two years, the aftermath of continued post-COVID stimulus and tighter monetary policy have worked steadily against each other.

When the Federal Reserve finally began raising interest rates in March 2022, financial markets and economists set their expectations for a quick downturn that has never arrived. Economists expected that after 12-18 months we would quickly see a mild but quick drop into recession. However, with the built-up strength of the consumer, that quick fall has yet to happen. Perhaps the best analogy for what has happened – in both the US and Houston – is that the economy took the escalator down instead of the elevator.

In fact, the long ride down is probably now ending as the economy finally seems to be normalizing and returning to pre-COVID trends. This is finally visible in both US and Houston households with incomes, employment, and spending all showing signs of a return to normal pre-COVID patterns. The question remaining is what happens when we get to the bottom of the escalator? Do we just walk off into a soft landing and resume pre-COVID growth like it was 2020 again, or do we trip and find a harder landing than expected as recession finally arrives?

The US Economic Outlook

For the short-run US forecast we rely on the Survey of Professional Forecasters. The SPF is the oldest quarterly survey among US economic forecasts. It was compiled and published by the NBER from 1960 to 1990, when the Federal Reserve Bank of Philadelphia was asked to take it over. Its results are published quarterly on the Philadelphia Fed website.

Participation in the survey is geared to 35-40 professional macroeconomic forecasting groups in academics, consulting, banking, and industry. Compare this to the general survey of National Association of Business Economics membership who may or may not be forecasters or to the heavy financial-sector participation of the Wall Street Journal’s outlook survey.

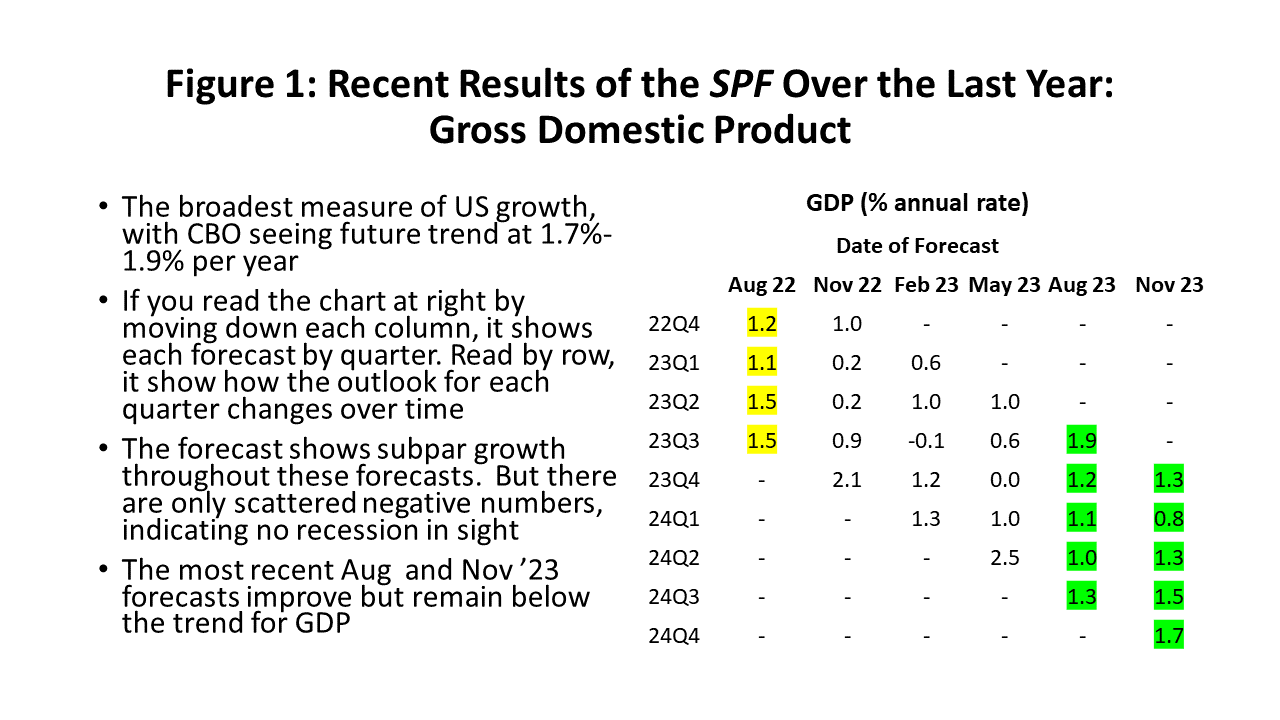

Despite sharply rising rates, the SPF has not forecast a recession in this round of tighter monetary policy. Figure 1 shows the results of the Survey over the last six quarters for gross domestic product (GDP), the broadest measure of the economy. Forecast results are shown for six quarters, allowing us to compare August 2022 to the latest SPF forecast available.

We saw a moderately strong economy in mid-2022, then an economy that was assumed to weaken through May, but which has now shown a return to better growth over the last two quarters. If we average the four forecast quarters in each SPF release this year, we see GDP growth increase steadily from 0.9 percent to 1.0%, 1,2%, and now 1.3%. This still runs below the long-run trend growth of 1.6-1.7% but looks more and more like the Fed’s soft-landing with a cyclical slowdown but no recession.

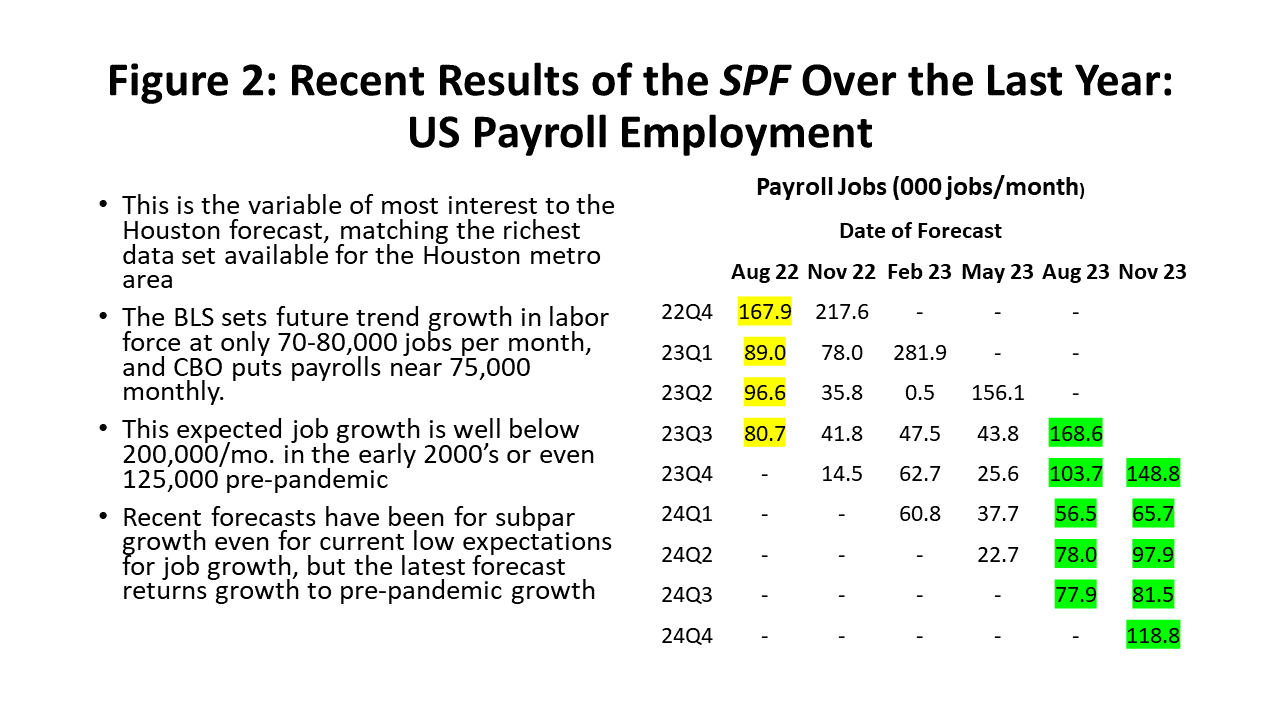

The US economy probably accounts for over 60 percent of the cyclical change in Houston, and the US variable we rely on most heavily for Houston’s forecast is US payroll employment. Regional economic data is limited compared to the wide-ranging and detailed data available for the US. In Houston, GDP and personal income figures are published only once a year, for example. Payroll employment, in contrast, is available monthly and provides substantial detail for comparison to Houston.

Figure 2 follows the format of Figure 1, except now substituting US payroll employment. A typical number of monthly US jobs over the dozen years leading up to the pandemic was about 125,000. Like GDP, job growth had already weakened by the August forecast of last year, weakened further in following quarters, but then strengthened again this summer. It currently shows the next four quarters running at an improved 91,000 jobs per month. Even with this improvement, we still see coming quarters running below trend job growth, although with no recession in sight.

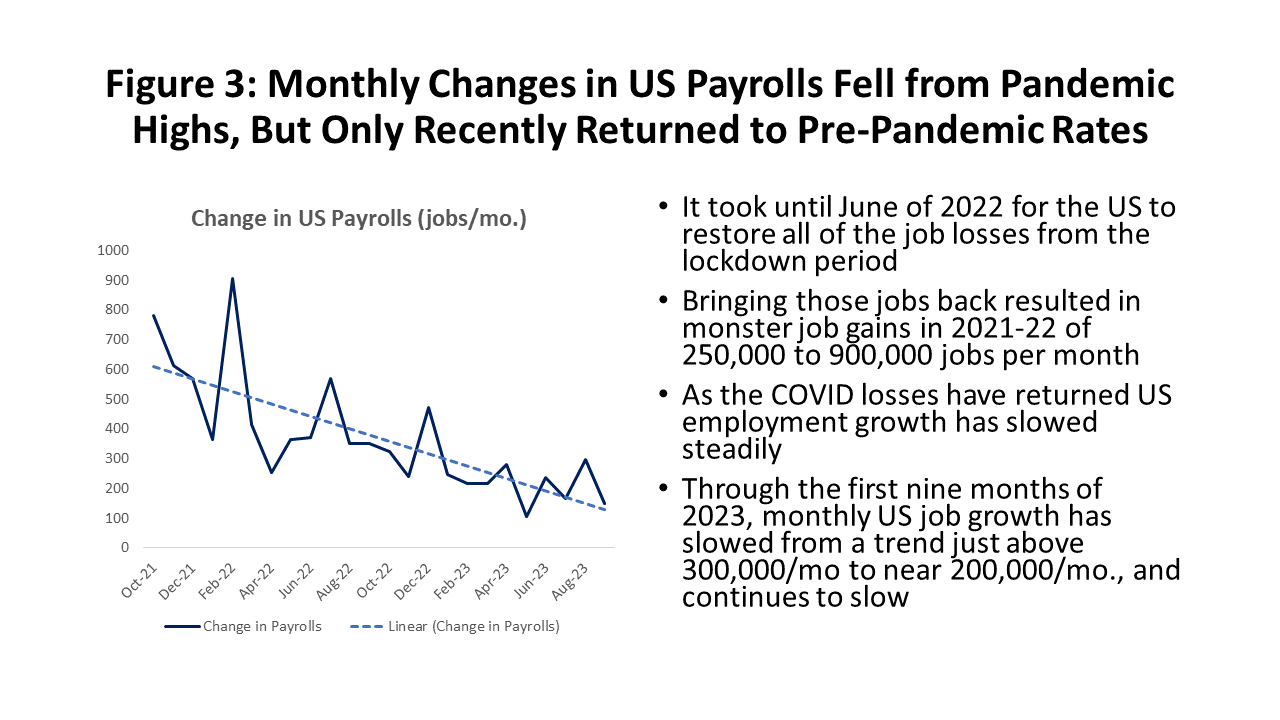

The most striking feature of these recent forecasts, however, is the persistence of job growth at quite high levels throughout the last year. And the persistence of the SPF membership in wrongly forecasting a sharp slowdown in the face of sustained and outsized job-growth numbers. In Figure 3 we can see that the SPF was certainly in too much of a hurry for slower growth to arrive, but that growth has been slowly falling for some time and returning to trend in both the US and Houston. Figure 3 is a nice picture of the escalator taken down instead of the elevator. Their forecast is for further moderate slowing to below trend but no recession.

This continued unexpected consumer strength is witness to the size of the stock of accumulated cash during the pandemic. (Discussed at length below.) However, this time the forecasters may be right. The US economy has already weakened on a number of fronts. Both US and Houston manufacturing fell into recession in mid-2022 and the wholesale trade sector quickly followed. Even quicker declines came from interest-sensitive sectors like single- and multi-family housing, commercial real estate, and banking. It was the large consumer sector that had refused to buckle under high interest rates, but signs of slower growth is now showing up in both income and spending, as well as jobs.

The End of COVID Stimulus … And How the Consumer Keeps Spending

The COVID pandemic is over, but the consequences of the policy measures taken to fight it remain central to the US outlook. The key economic problem in today’s economy remains inflation, with the CPI breaking out of its two-percent range in March 2021 following closely on the heels of the second and third rounds of fiscal stimulus. Year-over-year headline CPI inflation reached 8.6 percent by June 2022.

While the later rounds of fiscal payments set inflation firmly on its upward path, the Federal Reserve pushed the accelerator with zero interest rates held too low and for too long. Very low rates were maintained throughout 2021 while the Fed attributed the early inflation to a breakout to post-COVID supply-chain issues. A tremendous financial boom through 2020-21 used this low-rate environment to add as much as $15 trillion to household balance sheets before the Fed reacted and began to tighten monetary policy in 2022.

The fiscal stimulus came in two waves of $2.5 trillion dollars each, first in early 2020 during the lockdowns, then followed by two smaller rounds in late 2020 and early 2021 that together totaled another $2.5 trillion. Two and a half trillion dollars was about $16,800 per US household in 2020, and each round saw half or more of that cash flow to individuals directly or indirectly -- but quickly and as needed. Most went into the bank accounts of households and businesses through economic impact payments, the paycheck protection program, and enhanced unemployment checks.

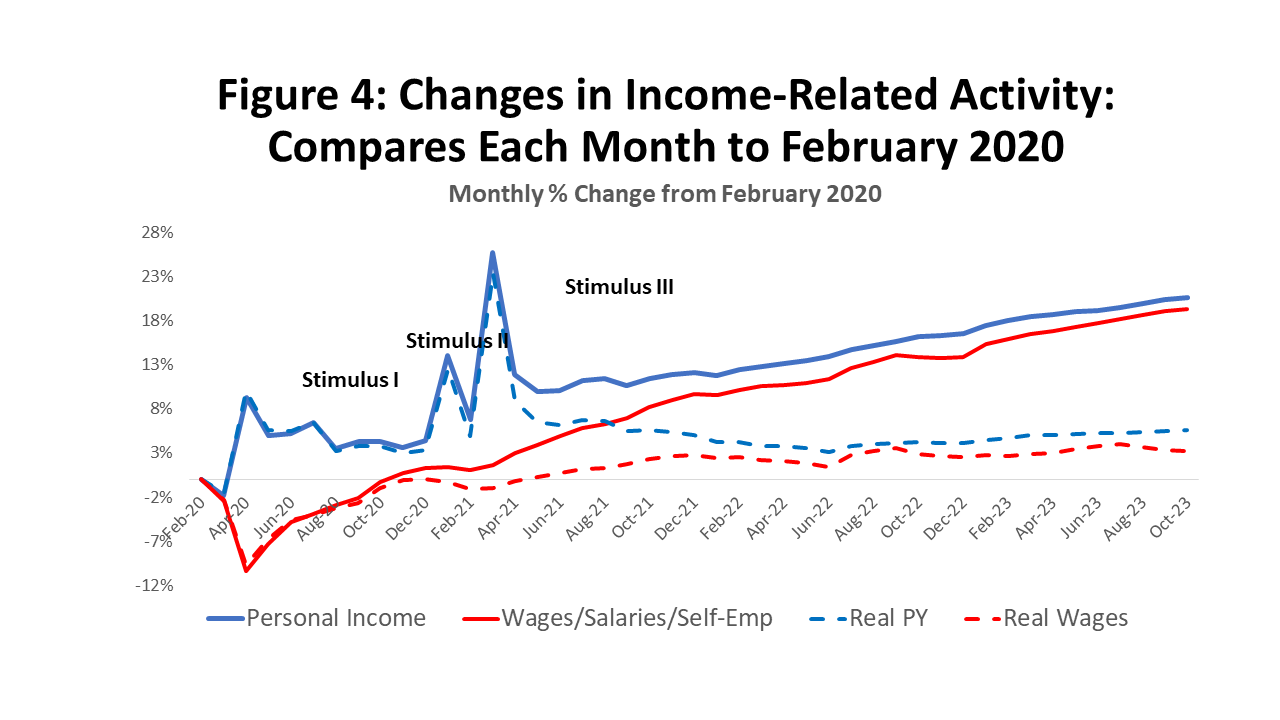

In Figure 4, the solid blue line shows the pandemic-period track of total personal income (including stimulus), and the solid red line is the wages, salaries, and income of the self-employed (no stimulus). Each point compares these measures to pre-pandemic levels in February 2020. The initial round of stimulus came against a backdrop of consumer shock and lockdowns, along with a ten percent drop in wages and salaries that was immediately matched by a ten percent jump in stimulus-driven personal income. These cash payments appeared to quickly right the economic ship by mid-2020 by offsetting wage losses and delivering record levels of income. Pre-pandemic levels of wages and salaries were fully restored by November 2020.

Figure 4 also shows us an economy that is now expanding on its own. The red line for wages and salaries has been growing rapidly since late 2020 and now stands 20.5 percent above pre-COVID levels. The blue personal income line has slowed as the stimulus recedes, although it is now being carried forward nicely by wages and salaries and is 19.3 percent above pre-COVID. However, the gains are much less impressive if inflation is removed as shown by the broken lines. Personal income is then up only 5.6 percent over three-plus years and wages and salaries up only 5.2 percent, or at annual rates of 1.5 and 0.9 percent per year since the lockdowns. The twenty-year trend before COVID for real personal income was 2.3 percent.

After the impact payments had been sent out to individuals, the major features of pandemic spending were the paycheck protection program and enhanced unemployment compensation. In April 2021, these programs were running at annualized rates of $763 billion, but by January 2022 all of the major programs were rapidly winding down and had largely ended.

How does spending continue at high rates? We know that the strength of the roughly 70 percent of the economy driven by consumers has been central to the strength of the overall economy. Fed rate hikes have slowed manufacturing and wholesale trade and most interest-sensitive sectors like housing. But for much of the last two years, Fortress Consumer seemed impregnable with sustained strength in income, jobs, and spending.

The on-going decline of Fortress Consumer was already illustrated in Figure 3 with the slow but steady fall in US employment growth as it returned to trend levels. Figure 4 just showed us that personal income adjusted for inflation is also now running well below trends. Figure 5 below perhaps does a better job of illustrating this on-going weakness in household income. Fiscal stimulus kept real personal income well above long-term trends through 2021 and until April 2022, when income fell below trend to stay. Real income sagged badly through early 2022, then attempted a recovery through May of this year before falling back again. The monthly declines since May have been persistent but still add up to less than one percent.

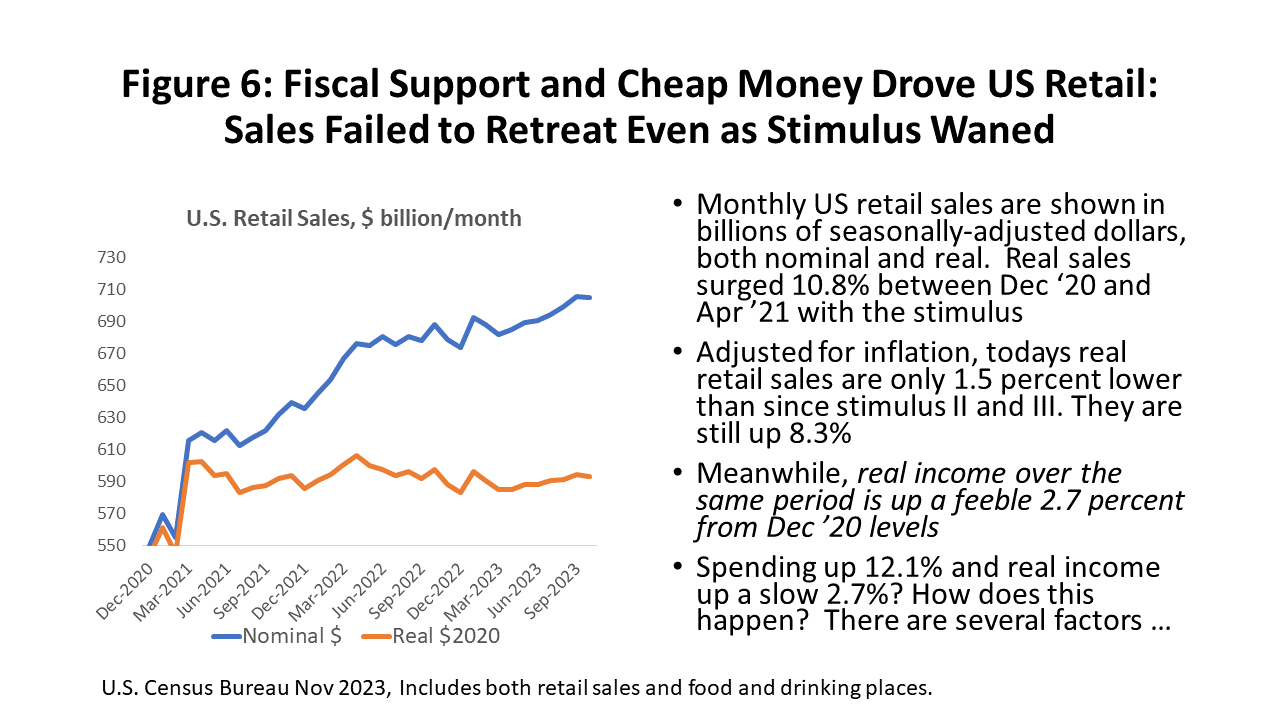

Real and nominal US retail sales since December 2020 are shown in Figure 6. The second and third round of stimulus arrived in late 2020 and early 2021, and real retail sales surges 10.3 percent between December 2020 and the following April. While the inflation-adjusted sales probably peaked in April 2022, they have fallen back by only 2.1 percent, giving up a small part of the extraordinary gains from stimulus. Meanwhile, real after tax income fell back 3.2 percent from December 2020 levels, providing support at only the weak levels seen above.

Our problem is simple: While the economic fundamentals for jobs and income continue to weaken, what keeps spending high? Is this support over? If not, how long will extraordinary spending last? Several factors come into play to complicate any simple answer to these questions.

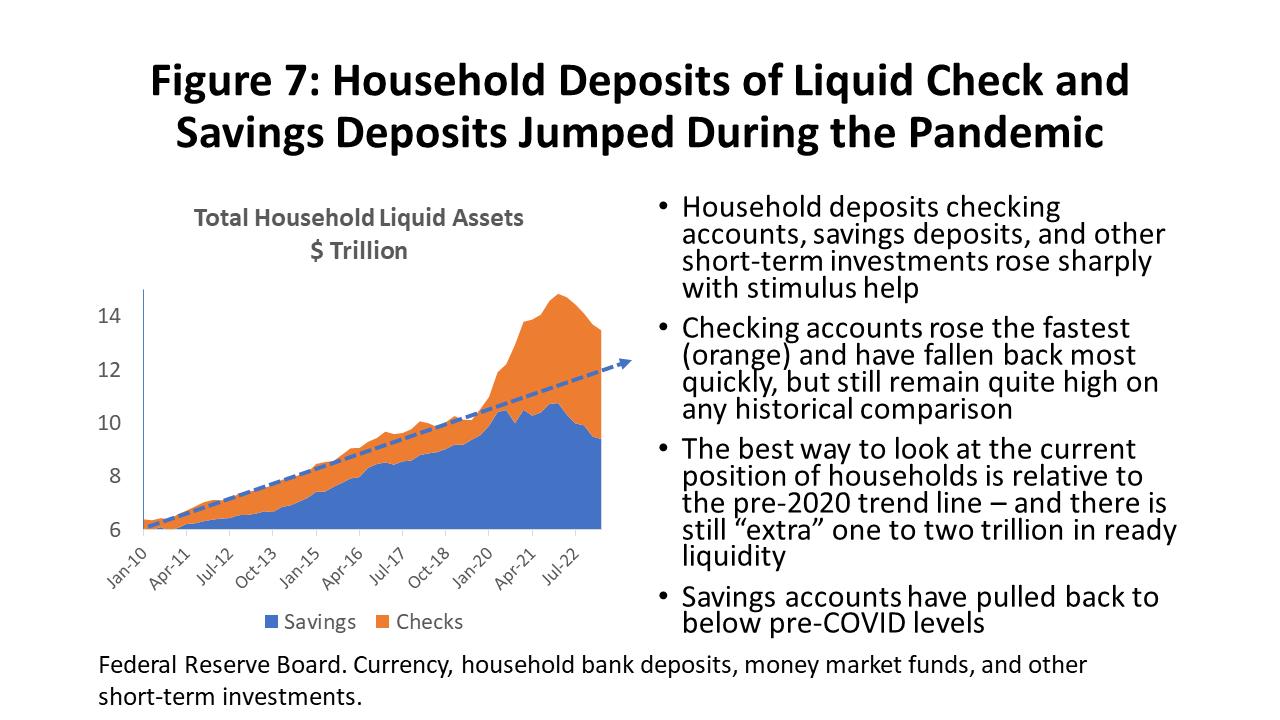

- While early rounds of stimulus were vital to protecting the US economy, much of the later rounds simply stacked up in household bank accounts as extraordinarily high levels of liquid assets that allowed households to continue spending freely after high stimulus levels ended. (Figure 7) Even as monetary policy slowed interest-sensitive sectors such as new and existing housing, commercial real estate, manufacturing, and wholesale trade, the 70 percent or so of the economy made up by the consumer continued to remain resilient.

- These measures of highly liquid excess savings are from the Federal Reserve Board’s household balance sheet and show holdings in checking accounts, savings deposits, and other short-term investments. Pre-COVID holdings were around 10 trillion dollars, they peaked at over $14 trillion, and have fallen back to only $12-13 trillion. Even allowing for trend growth since COVID, there is still probably between one or two trillion in readily available liquidity.

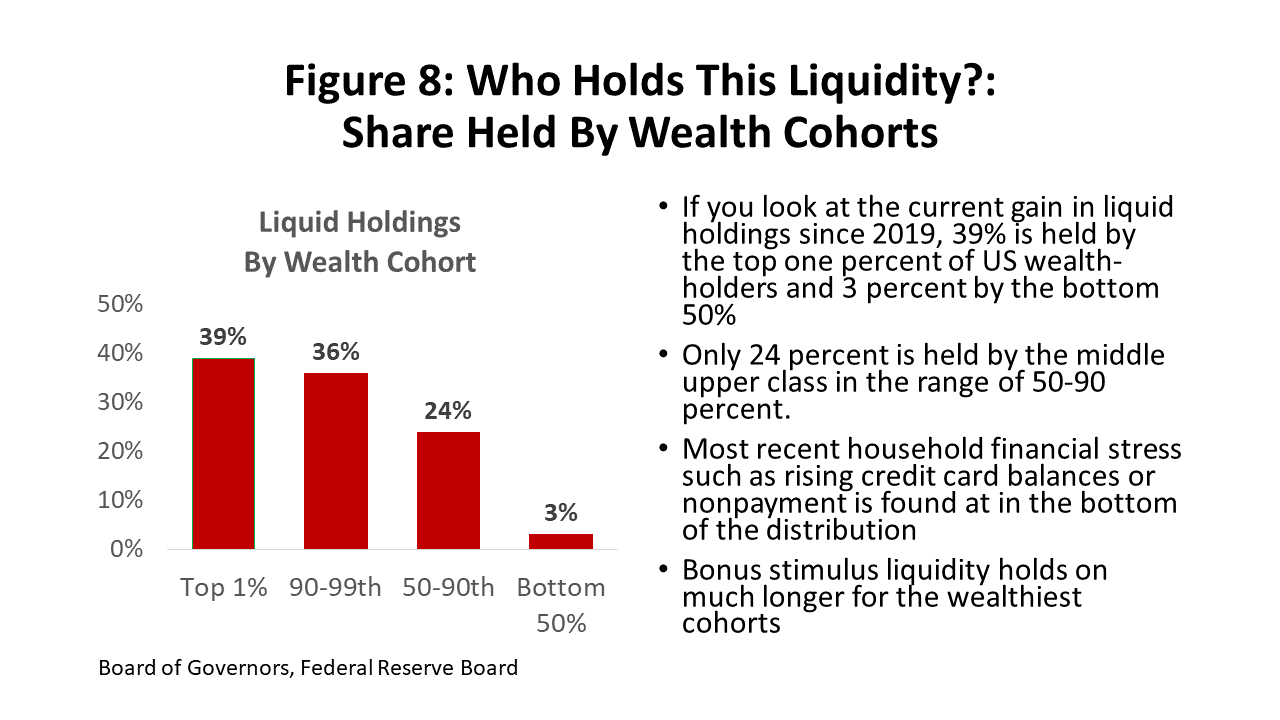

- Another complication arises if we ask who holds these liquid assets. Figure 8 shows the distribution of liquid assets by wealth cohort, with the bottom 50 percent now holding only three percent. Given the initial stimulus payments were heavily geared to the bottom of the income distribution through impact payments, payroll protection, and unemployment compensation, this was the money spent first. The mystery is the heavy holdings of $1-2 trillion of liquid assets by the top 50 percent – especially checking -- unless they still intend to spend it soon.

- Despite paying the highest interest rates since the 1980’s, credit card debt has returned to an all-time high. Any financial stress again should stem from the bottom of the wealth holdings. Overall household debt remains manageable, however, and credit cards are a relatively small share of this debt. However, “manageable” depends on a continued strong income and employment situation for these borrowers.

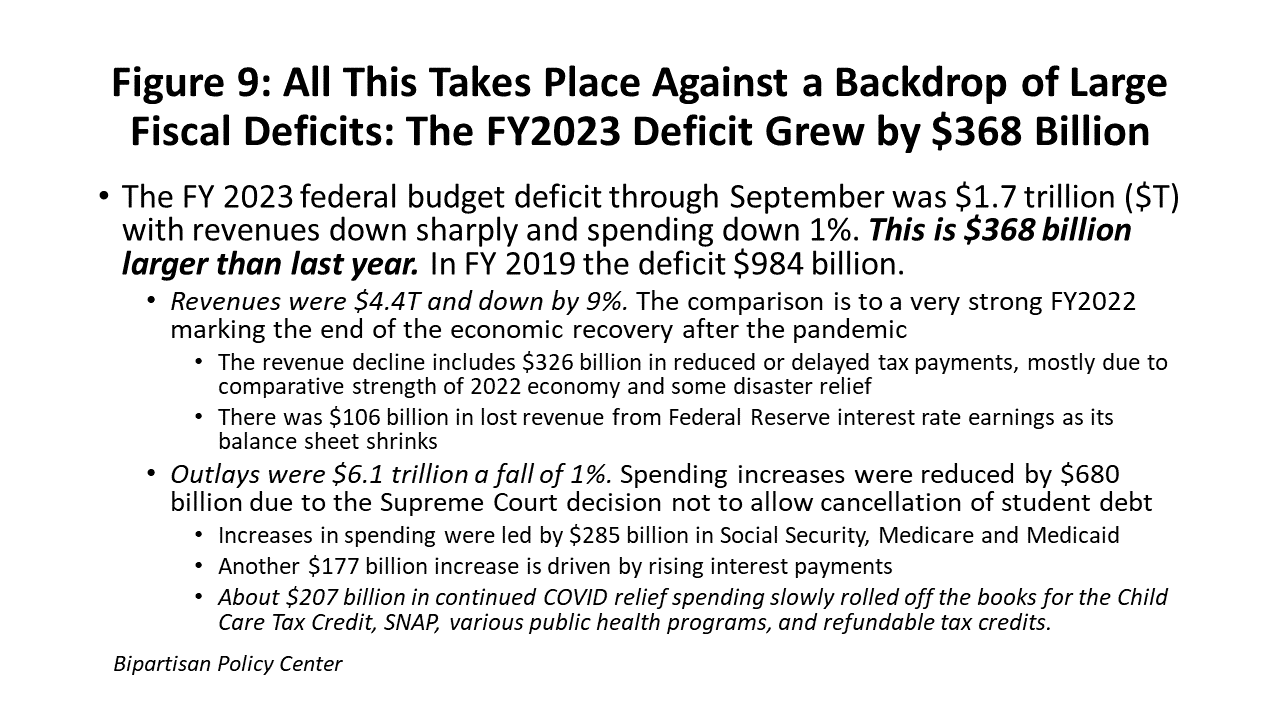

- Finally, it should be noted that the COVID stimulus actually continued at comparatively low levels through FY 2023 as the final $203 billion rolled off the books. Nor was the COVID spending the only deficit spending underway. According to the Congressional Budget Office, the Inflation Reduction Act (IRA) – a large infrastructure bill that was passed in August 2022 -- will add $305 billion to the US fiscal deficit by 2035, and this spending is only now gaining momentum as projects are authorized.

- Finally, the FY 2023 fiscal deficit, helped along by COVID and the IRA, added $368 billion to the previous FY 2022 deficit of $1.7 trillion. (Figure 9) In pre-COVID FY 2019, the deficit was $984 billion. We have gotten used to federal spending measured in trillions, but $369 billion still has provided a meaningful boost to recent economic growth. This spending has left Fed monetary policy working steadily uphill as it tries to slow the economy and inflation.

The Federal Reserve Waits for the Economy to Catch Up

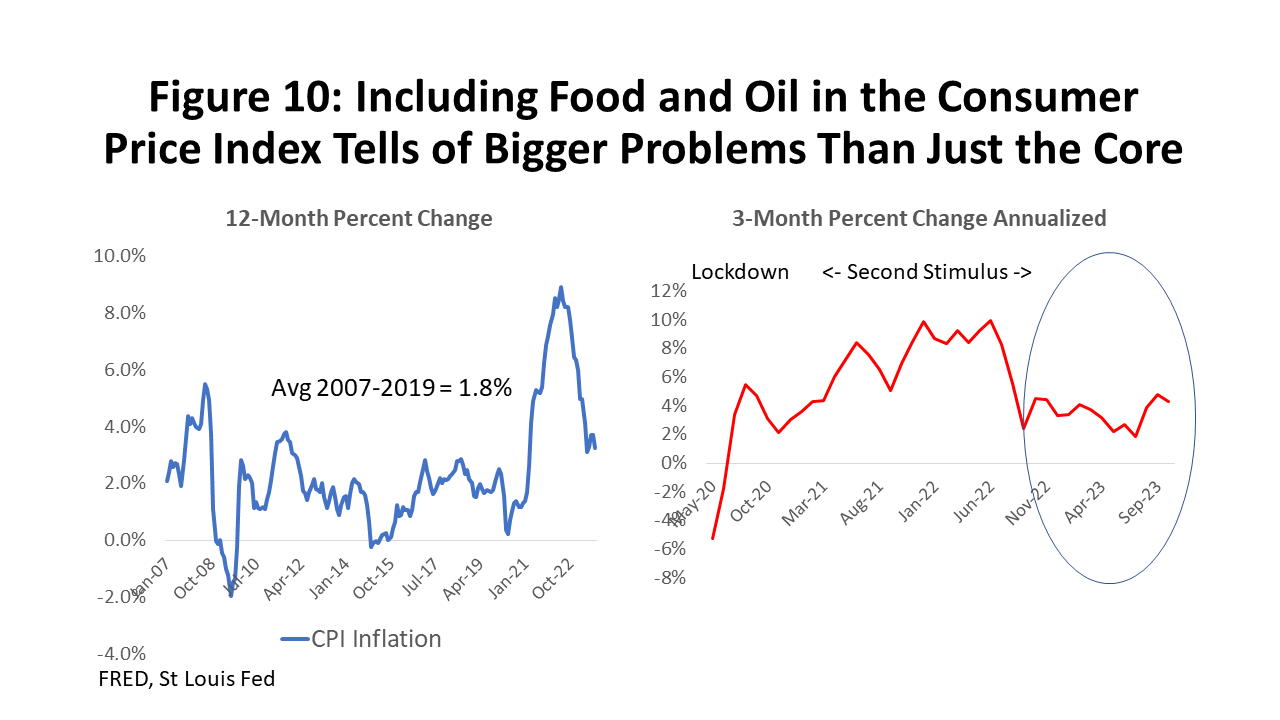

The recent outbreak of inflation began in earnest in early 2021. After 15 years of the Federal Reserve failing to push inflation high enough to meet its 2.0 percent price target, 15 months later CPI inflation was peaking at 8.6 percent based on 12-month annual changes. (Figure 10) Rising oil and food prices following Russia’s invasion of Ukraine contributed strongly both to the CPI peak and the fall to 3.2 percent. On the basis of 3-month changes, the CPI was recently running as slow as 2.0 percent annual rates as oil prices declined, but it has now reaccelerated and by October stood at 4.3 percent.

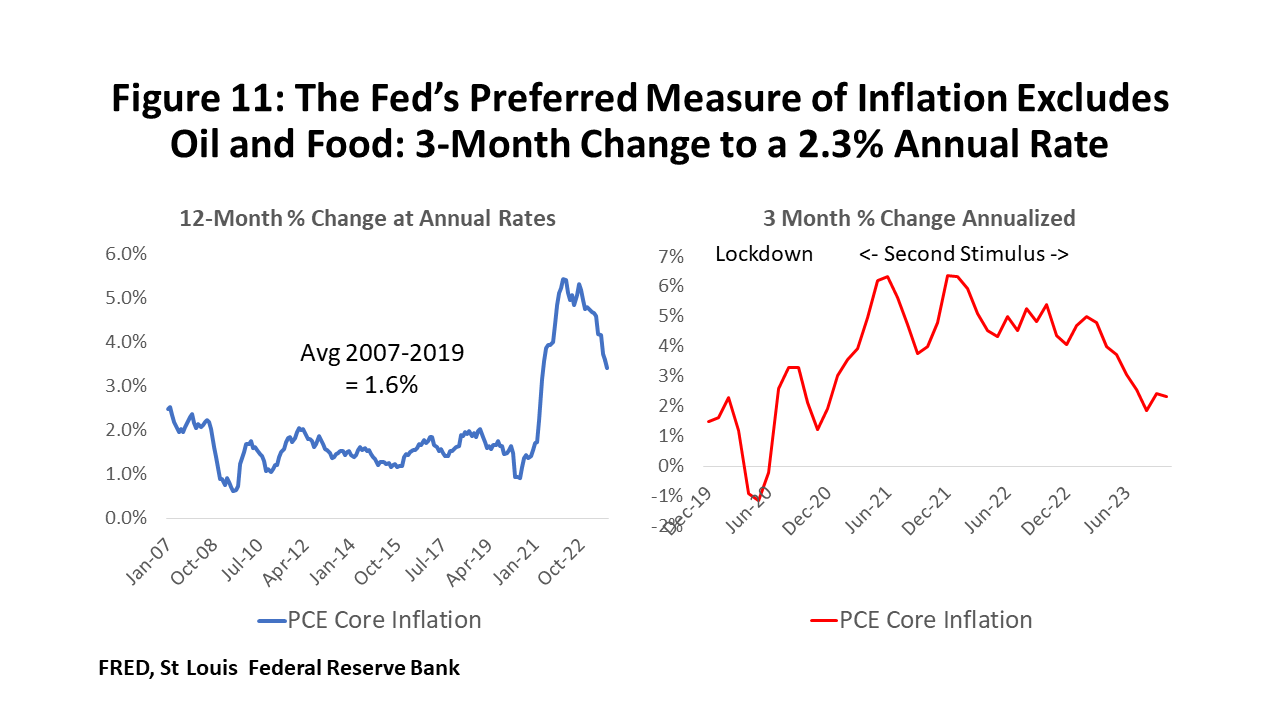

For policy purposes, however, the Federal Reserve uses another measure of price change and inflation. It turns to the personal consumption expenditure (PCE) deflator from the national income accounts, with a methodology more trustworthy than the CPI. Alan Greenspan -- and many others -- have called the CPI a “deeply flawed” measure of price change. Further, the Fed excludes volatile oil and food prices from its price calculations because oil markets and crop failure are well out of the Fed’s span of control.

Figure 11 shows the core PCE at work. Like the CPI, for 15 years it failed to meet the two percent Fed target, and the PCE breakout and inflation peaks were timed much like the CPI. However, this time the Fed’s core PCE saw prices rise to only 5.4 percent peak or 3.2 percent below the CPI peak. While these lower prices are of little comfort to the consumer who lives with the reality of recent food and gasoline inflation, this is the measure the Fed watches closely for purposes of steering monetary policy.

Until early this year, progress was slow in bringing down prices as measured by the core PCE. Based on the 12-month changes in the left side of Figure 11, prices now have fallen from the 5.2 percent peak to 3.4 percent. However, using 3-month changes (right side), the October data show a fall to an annualized rate to 2.3 percent. Progress all comes this year, and the three month change is not enough to provide any certainty they will stay this low, but it is a promising near-term trend that we hope continues to hold.

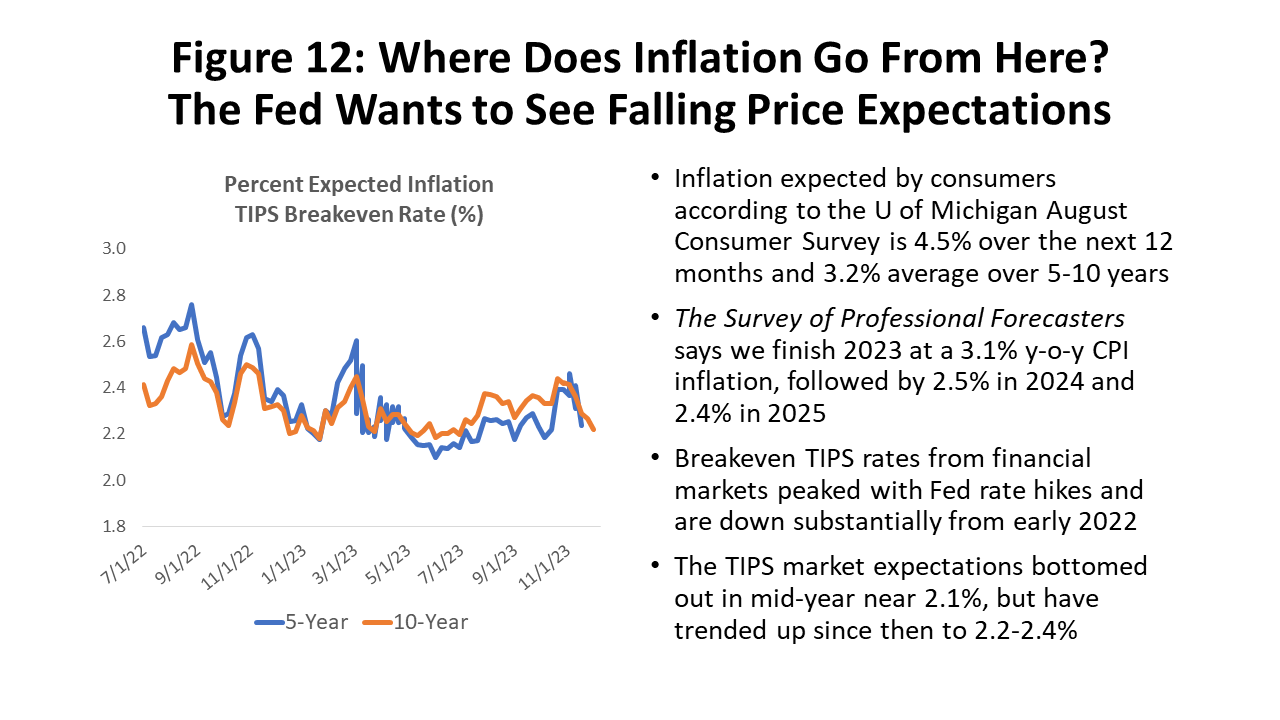

We continue to get mixed reports on expectations of inflation. Inflation expectations can become self-fulfilling and can slow the disinflation process, e.g., through collective higher bargaining demands. Consumers are always the least optimistic group, and this is reflected by the University of Michigan’s monthly survey of household price expectations. (Figure 12) Consumers currently see prices running 4.5 percent over the next twelve months and 3.2% over the coming five to ten. The SPF sees inflation running 2.4-2.5 percent over the coming 12-24 months. And by looking at the implied inflation rates from the market for Treasury inflation-protected securities (TIPS), financial markets expected inflation to fall from a 2.4-2.7 percent in late 2022 to a range of 2.2 to 2.4 percent today.

But none of these expectations have quickly settled into the Fed’s two percent goal -- which directly questions the central bank’s credibility as an inflation fighter. Similar doubts about Fed resolve can also be seen in financial markets. As the market continues to think that the Fed will back off and cut rates at the first sign of weakness in the economy.

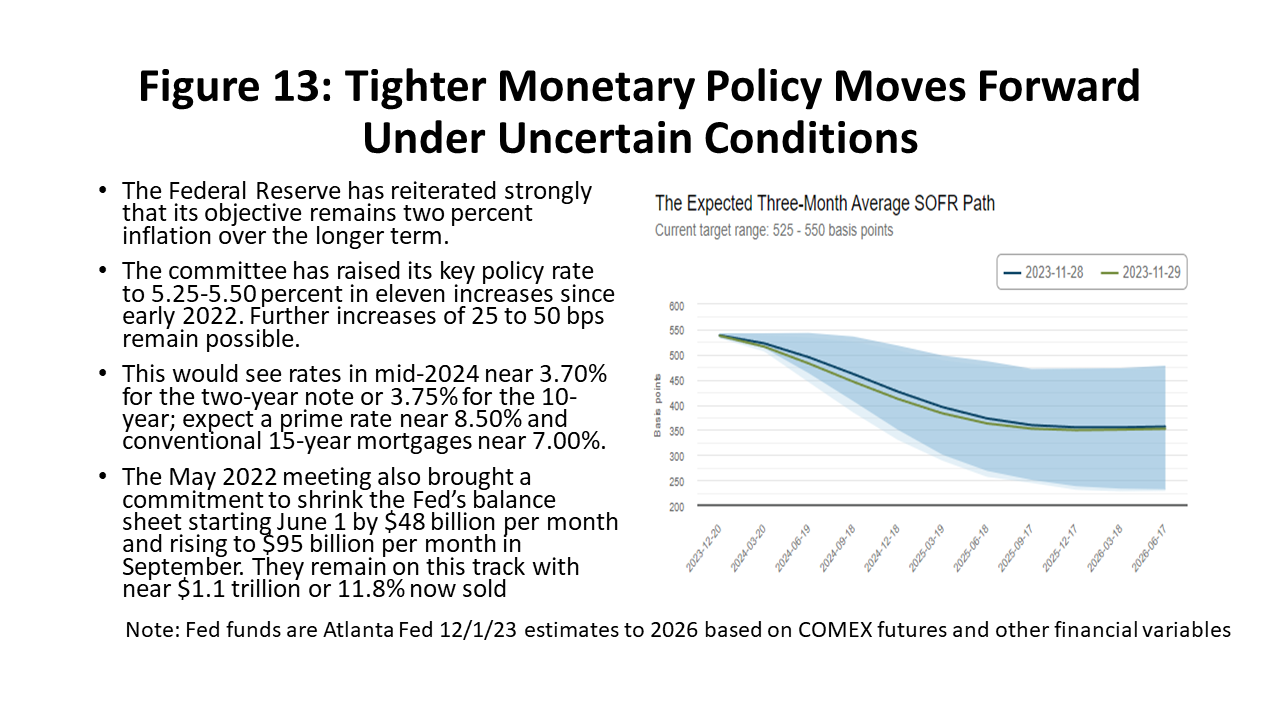

The chart in Figure 13 is a market-based Atlanta Fed forecast of the federal funds rate using the COMEX futures market and international swaps, and it reflects market doubts about Fed conviction. First, note that expectations are for a series of rate cuts beginning in early 2024 and continuing, running counter to the Fed’s public statements. Second, note that even through 2025 the forecast policy rate remains high, ending the year near 3.7 percent. If we combine the Fed’s internal estimates of its long-term real interest rate at 0.7-0.9% with the market’s 3.5 percent policy rate through 2025, it implies inflation running near 2.6 percent, i.e., 3.5% - 0.9% = 2.6%. This remains well above the Fed’s 2% target and again shows the market’s doubts about the Fed’s willingness to do what is necessary to meet the 2% target.

Can the Fed break the back of consumer spending, slow the economy, and bring inflation down? They certainly have the tools, and it is political will that the market questions. The Fed tried a timid campaign to restore a positive policy rate from 2016-2019, slowly raising rates from 0.5 to 2.5 percent, but then quickly cutting rates in early 2019 at the first signs of economic weakness. Then came the pandemic, the restoration of zero interest rates, and a decision to hold these rates at zero for far too long after inflation broke out.

Embarrassed by this recent record, central bank credibility, personal legacies and professional reputations are at stake. I think the Fed is now prepared to do what is necessary to bring inflation down to its two percent target.

The Fed has stopped its steady series of rate increases and is now watching and waiting for further progress on inflation. The household sector as the remaining barrier to progress – income, employment, spending – and it must clearly weaken if inflation is to be definitively broken. As we already have seen in this report, employment and income have already fallen back to historical trend growth rates, while household spending continues to weaken but hold at high levels.

The Big Picture of Houston’s COVID Recovery

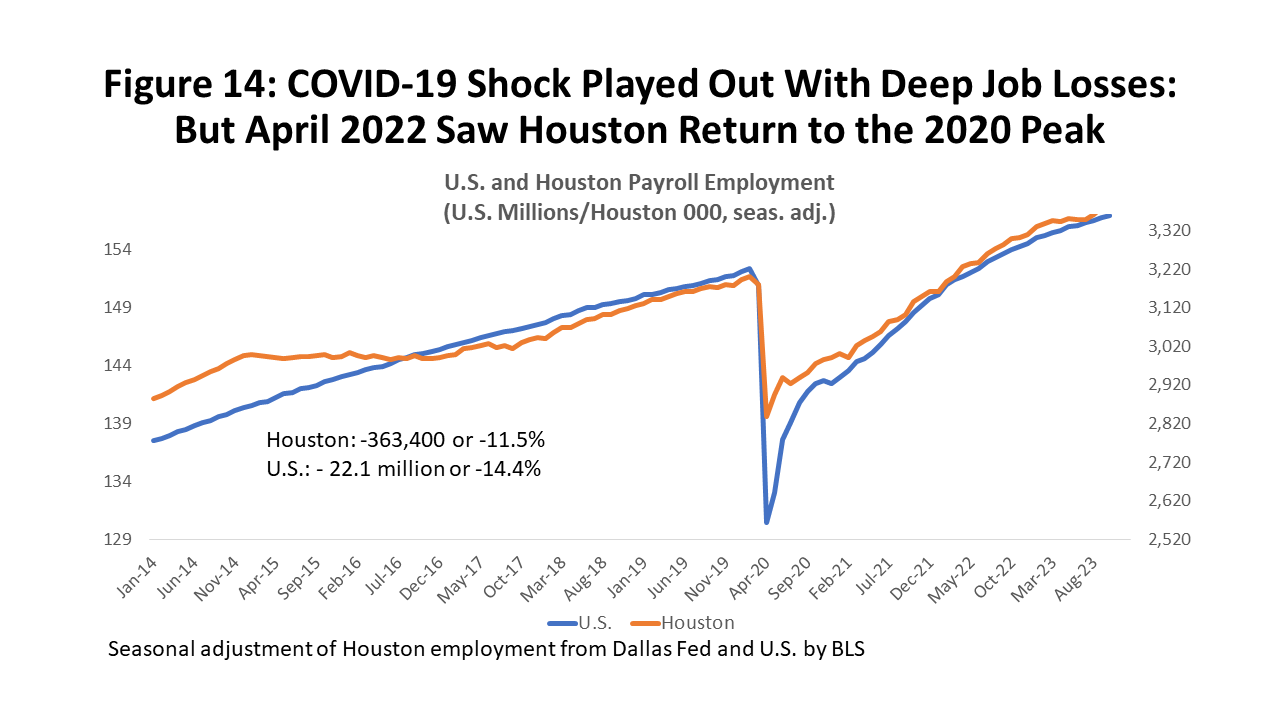

There is no question that Houston’s payroll employment has produced extraordinary growth in recent years. Its 2019 payroll employment growth was right on a typical trend pace of 58,400 or 1.7 percent. Then came the pandemic and the loss of 190,500 jobs year-over-year, the return of 163,900 in 2021, and finally another 150,400 last year. Once pandemic-era jobs were restored to their prior peak last April, Houston moved into a new economic expansion and has since added another 178,800 jobs.

But we need to be careful in how we interpret these extraordinary job gains. First, cyclical recovery from a major downturn always should bring jobs back quickly, as labor and capital have been pushed to the sideline by recession. But as soon as demand returns, workers and factories are immediately available to return to work. And COVID left many jobs to bring back. Houston’s job return has been right in line with the deep lockdown losses and post-pandemic recovery seen across the nation which, above all, reflects the depth of losses forced by COVID. Recovery always slows sharply to an ordinary cyclical expansion once we must begin the wait for new workers to be trained or new factories to be built.

Houston’s payroll employment losses and recoveries are shown in Figure 14, with a two-month lockdown decline of 363,400 jobs or 11.5 percent. This compares to 21.1 million US jobs lost or 14.4 percent. Houston’s decline was smaller thanks to a less restrictive lockdown policy in Texas, and the stronger initial US recovery was a strong bounce back as heavier COVID sanctions were lifted. However, for the most recent recovery phase, Houston and the US were on virtually the same track.

By April, Houston had added back all of the lockdown losses, plus another 178,800 jobs through this October. The US completed its job recovery two months later in June. Note that since the job recovery last year, Figure 14 shows a broad slowdown in job growth as both the US and Houston curves slowly flatten.

Houston’s Economy Now

The Fed’s efforts to slow the US economy are having much the same effects on Houston as on the US: credit-sensitive sectors responded quickly and negatively to higher interest rates, manufacturing slipped into recession, and local wholesale trade jobs broke a strong growth trend in October 2022. We lack timely data on personal income or consumption in Houston and other metro areas, but spending in Houston now looks weaker than the US. Local employment growth has slowed sharply through the first 10 months of this year, following the US lead.

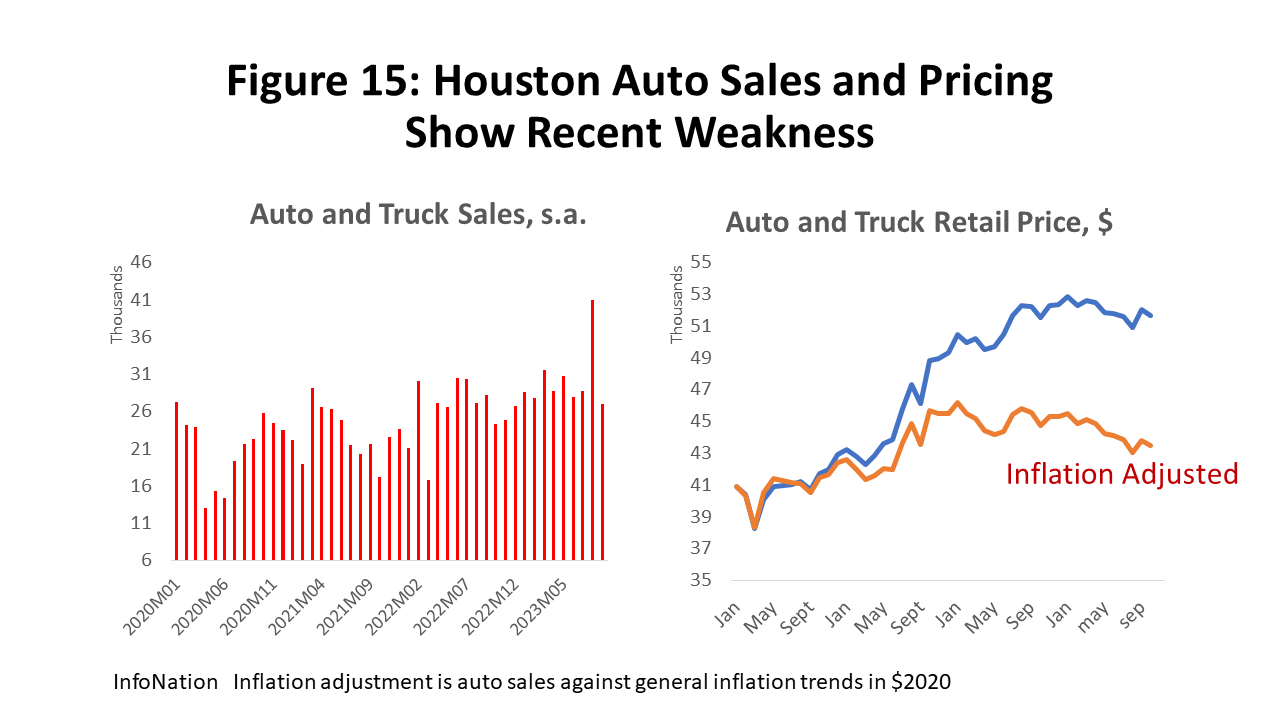

Autos and housing were affected in different ways by the pandemic and responded differently. Autos, for example, struggled to deliver product due to chip and other material shortages, choking supply chains, and making price the major outlet for surging auto demand in 2021 and early 2022. (Figure 15) The big supply kinks have since worked out; auto sales rose through late 2022 and the early part of this year but are now falling and are widely expected to fall further in the coming year.

Auto and truck prices remain high – still about 25 percent above pre-COVID levels – and prices peaked earlier this year and are now falling slowly If we recognize that inflation is up by about 20 percent since 2021, real prices for autos have been falling since 2021 and are up only 6.3 percent from pre-COVID levels.

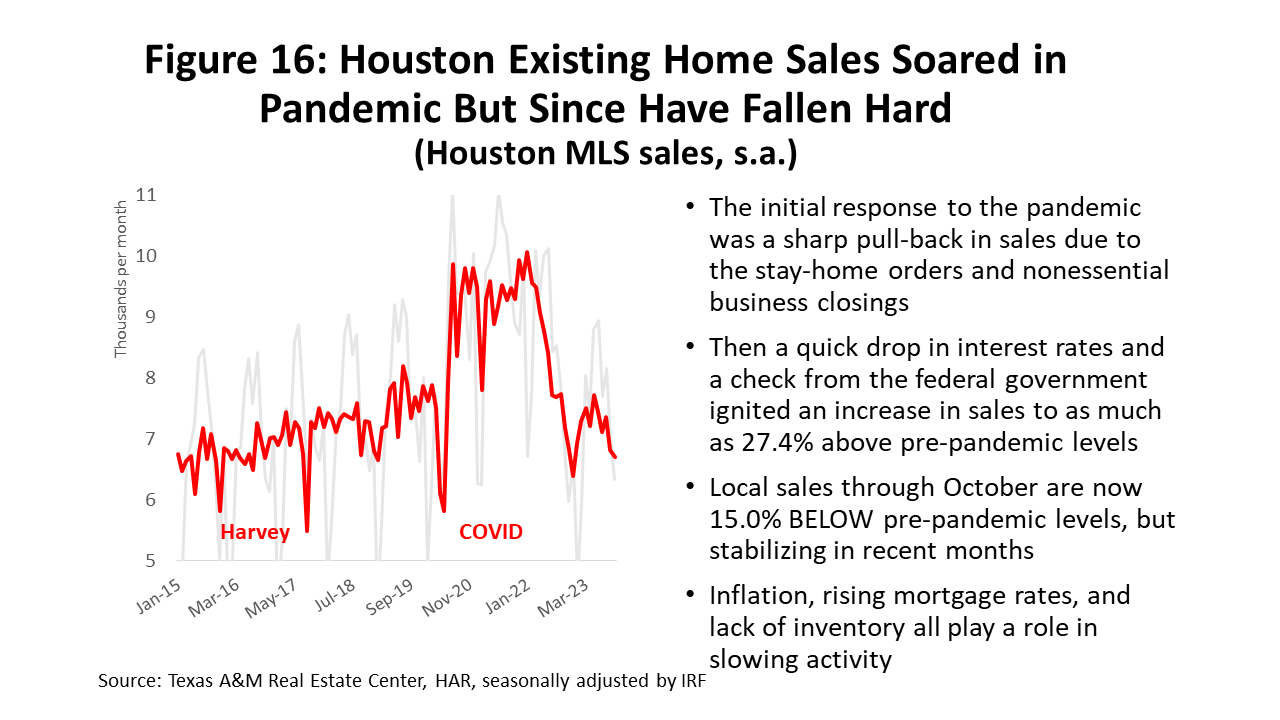

Existing home sales were a local pandemic bubble that burst as soon as mortgage rates began to rise. (Figure 16) Existing home sales in Houston fell hard during lockdown months but recovered quickly with a check from the federal government and zero interest rates. Housing became a major element of the 2021 financial boom. Sales in Houston rose as much as 27.4 percent above pre-pandemic levels, only to fall hard after the Fed rate hikes began. Sales then fell back as far as 19.0 percent below pre-pandemic levels and have since recovered only to 15.0 percent below.

Existing home prices surged from $250,400 for the typical unit to $344,100 during the boom period, or by 37.4 percent. So far, sharply falling sales have pulled prices back by only 3.3%, and history says prices could hang on to a big part of these gains in years to come. However, such an outcome would likely mean a decade or more of small or limited home price appreciation.

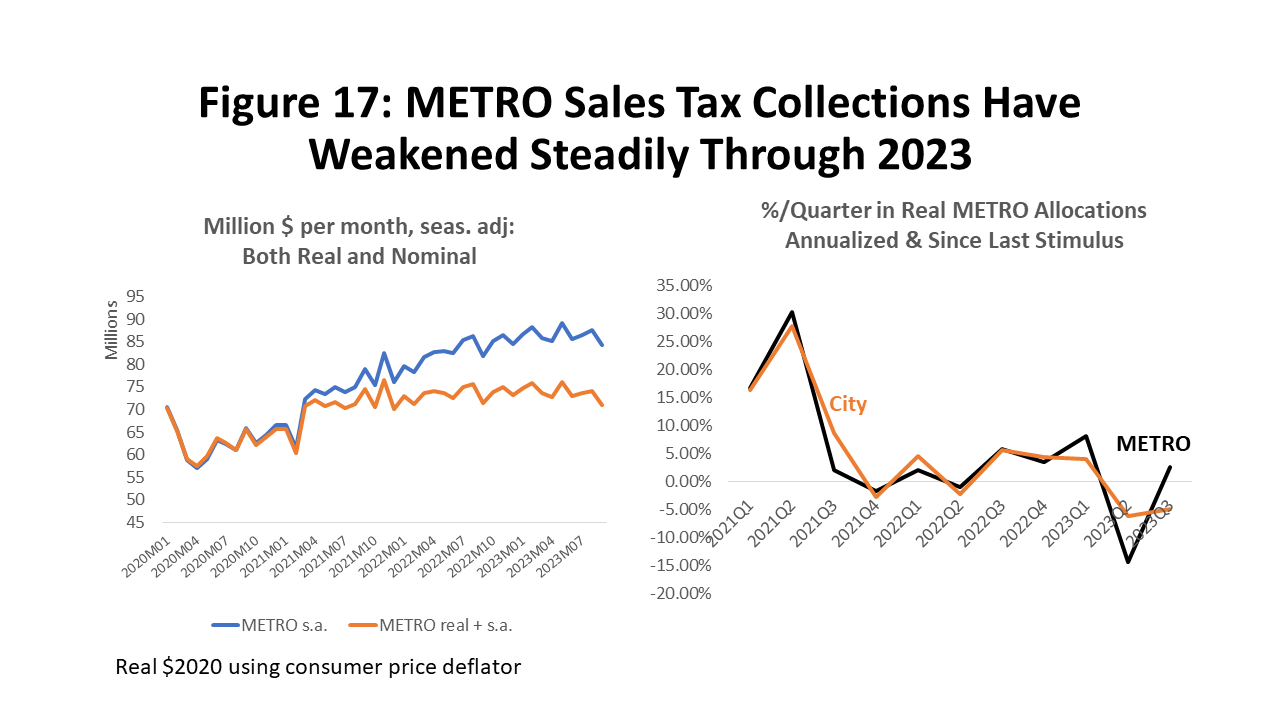

For Houston and other metropolitan areas, we do not get timely data on personal income or consumption, but spending data is available indirectly through sales tax collections by the City of Houston and METRO MTA. METRO MTA revenue provides a better window into these spending results, because they include all the City Revenues plus METRO’s longer reach into the suburbs. If you look back at Figure 6 on US retail sales and compare them to METRO’S sales tax collections in Figure 17, they are a mirror image of each other in many ways. Like the US, 2020-21 stimulus payments we see a sharp one-time jump in METRO’s sales tax collections of 9.8 percent or $6.5 million per month. This is the equivalent of $650 million dollars monthly in local taxable sales.

Even adjusted for inflation, these revenues have yielded little ground to this one-time surge above December 2020 levels. Like the US, Houston’s consumers are probably relying on past high levels of liquidity to keep spending. And high levels of local consumer spending have been an essential prop to keep the local economy running at high levels. The right side of Figure 17 compares the quarterly growth of inflation-adjusted allocations for METRO and the City of Houston, and both show considerable weakness and outright declines through the first three quarters of 2023. This matches other signs of slowing and emerging weakness across both the US and Houston.

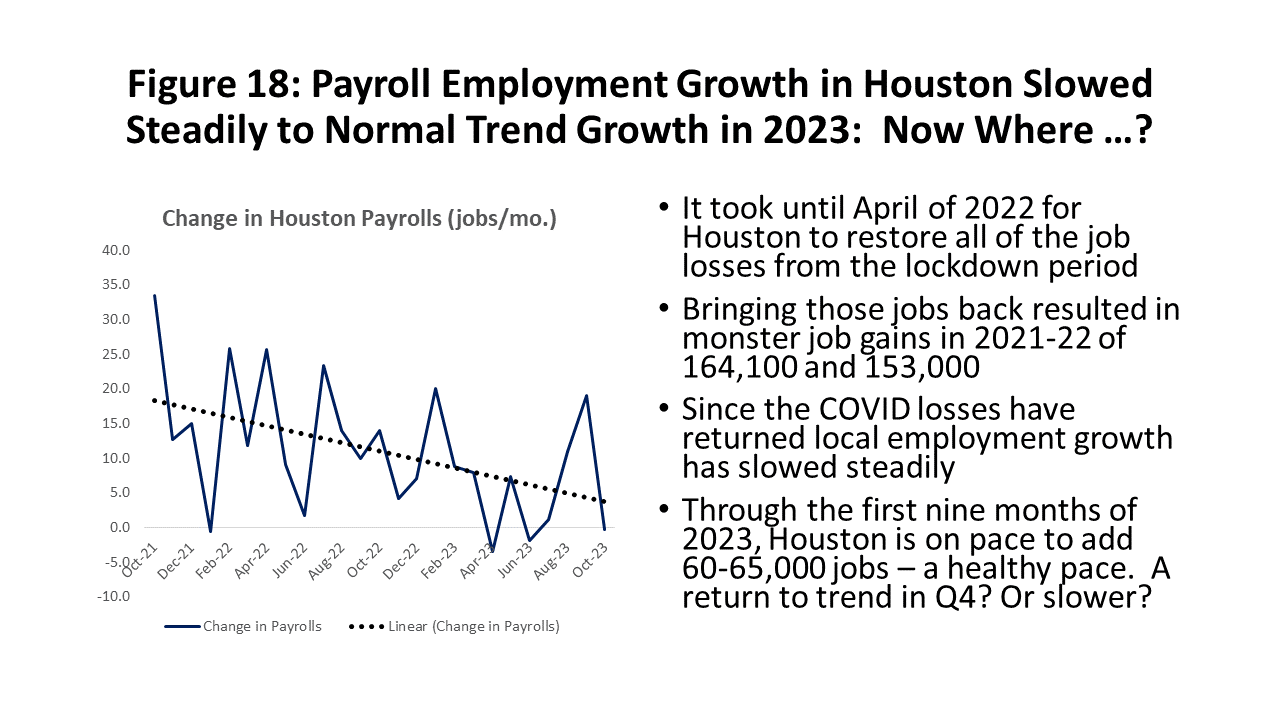

Figure 3 earlier showed the long, slow escalator ride down for US payroll growth, and Figure 18 shows the same chart for Houston. Results here are the very similar as the US. with Houston jobs moving under 5,000 per month in June. This monthly 5,000 jobs is 60,000 per year, or close to Houston’s current long-term trend rate of job growth, just as recent US job growth has entered a final post-COVID slowdown and moved back to monthly long-term trends near 125,000 per month. The Survey of Professional Forecasters expects this US slowdown to continue through 2024, and our forecast expects Houston payrolls will follow the US lead.

Houston Oil: Smaller, Cautious, More Stable

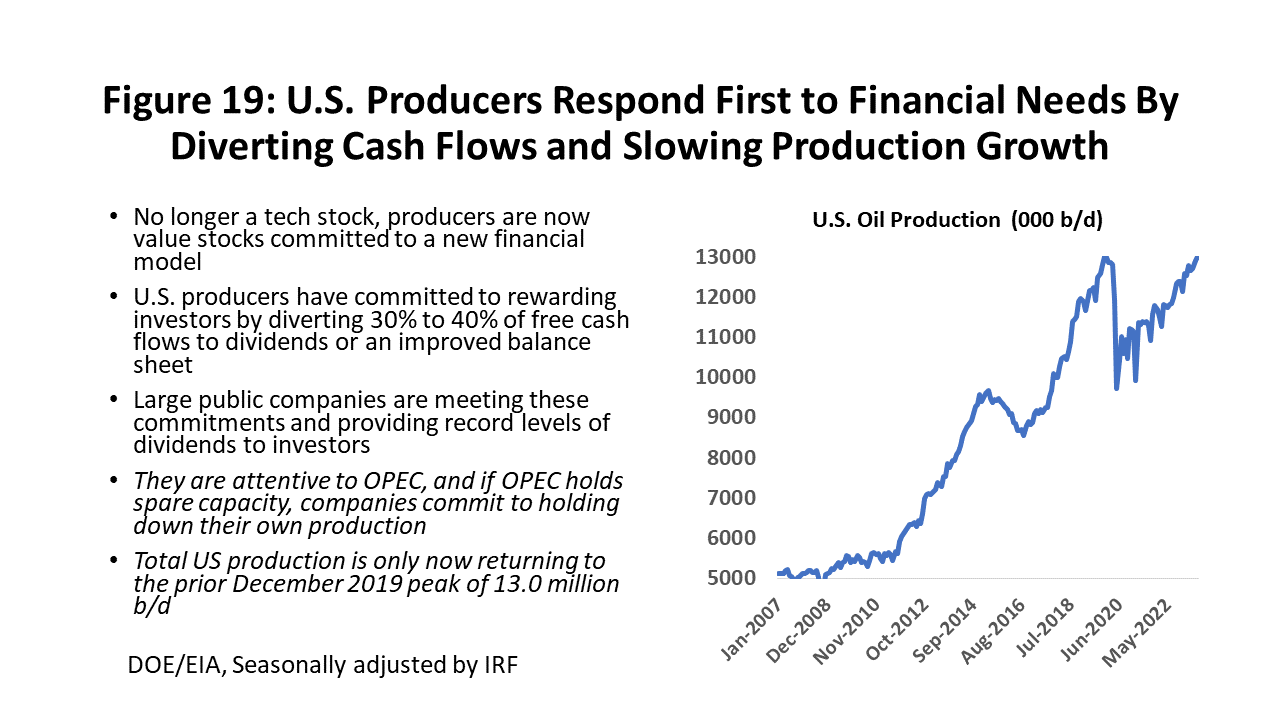

We have stressed in recent reports that the economic impact of oil on Houston is now smaller but more stable. The fracking industry has accepted that it is a high-cost source of oil and that it can no longer rely on sustained high oil prices and rising equity values to attract investors and finance oil-field activity. Instead, it has become a value stock committed to using 30-40 percent of operational cash flow to draw investors. This means dollars that once went to the oil fields now go to investors, and there is substantially less oil-field activity at every oil price than would previously have been expected.

The new financial model began to be widely adopted after the Saudi-Russian “Oil War” that was concurrent with the pandemic lockdowns in March 2020. The new rules of the road are summarized in Figure 19. First, there is a commitment to investors to pay significant dividends before spending in the oil fields. Second, there is an understanding that if OPEC holds substantial spare capacity, US producers will not raise production significantly. Since 2014, OPEC used three rounds of price cuts to discipline the US oil industry and to teach producers that fracking is a high-cost source of oil. The result was $300 billion in US fracking assets that passed through the bankruptcy courts, and a US oil industry that now watches and listens carefully to OPEC. Most public companies have committed to their investors that they will hold down production if OPEC holds spare capacity.

Oil prices increased to $70/b by late 2021, drawing strength throughout the post-pandemic era from a rapidly improving global economy, stronger travel demand, and increased power generation. OPEC first intervened again in oil markets in 2022 to cut production in the face of a weakening global economy. Since December 1, there are 2.0 million barrels per day of cuts underway within the official OPEC framework and another 2.2 million of “voluntary” cuts by Saudi Arabia, Russia, the UAE, and other producers. Their main effect has been to keep the price of oil near $75 per barrel.

According to the US Energy Information Administration, OPEC holds 3.4 million barrels per day of excess capacity and they project this to rise to 4.3 million in 2024. This is more than adequate for emergency use or other near-term needs to expand crude supplies. US production remains the primary source of new global oil supplies, but higher prices have brought a tepid response from the US. Production rose by only another 500,000 barrels per day through the first seven months of this year, and US oil production is only now returning to pre-COVID levels.

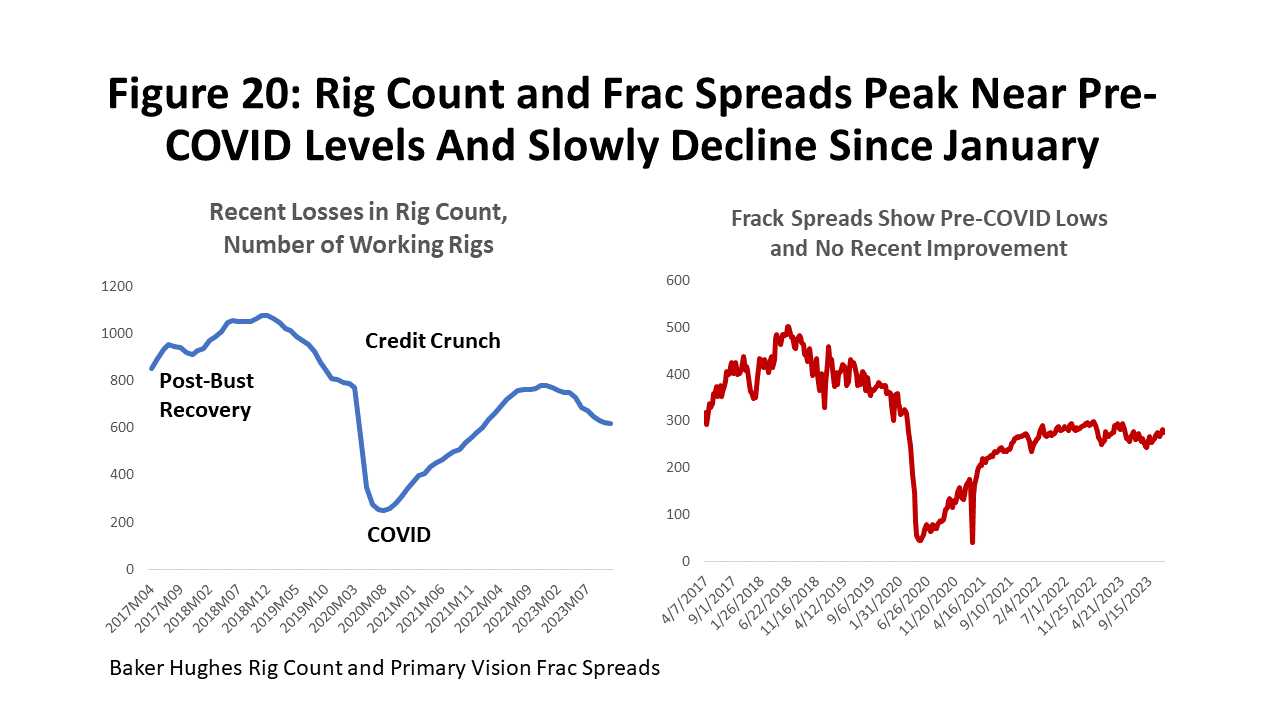

The combination of a new financial model and attention to OPEC spare capacity explains why there has been no rush back to the oil fields after COVID. (Figure 20) The rig count fell to near 760 before COVID arrived, and then rigs fell hard to an all-time low of 253 in the Saudi/Russian Oil War. Recovery saw a return to 780 working rigs before beginning to fall yet again, and they are now down by about 18 percent this year. Frac spreads are the more modern measure of activity in the oil fields, but they tell much the same story – well down from pre-COVID levels and 5.3 percent lower than this spring.

This decline in rigs and frac spreads has less to do with oil price than rising interest rates. For large public companies, the new financial rules are firmly in place with strict capital discipline and investors getting paid first. These large companies are also driving big gains in productivity in fracking, holding onto rigs, and accounting for most of the recent oil production increases.

The laggards are small private companies that can’t use the new model. Often relying on bank financing, they are now struggling with higher interest rates, lower-quality acreage, and an inability to capture the productivity gains of big competitors. They are shedding rigs, reducing drilling, and account for most current reverses. Cost escalation has stopped in the oil-fields, but high cost levels remain challenging for labor and supplies.

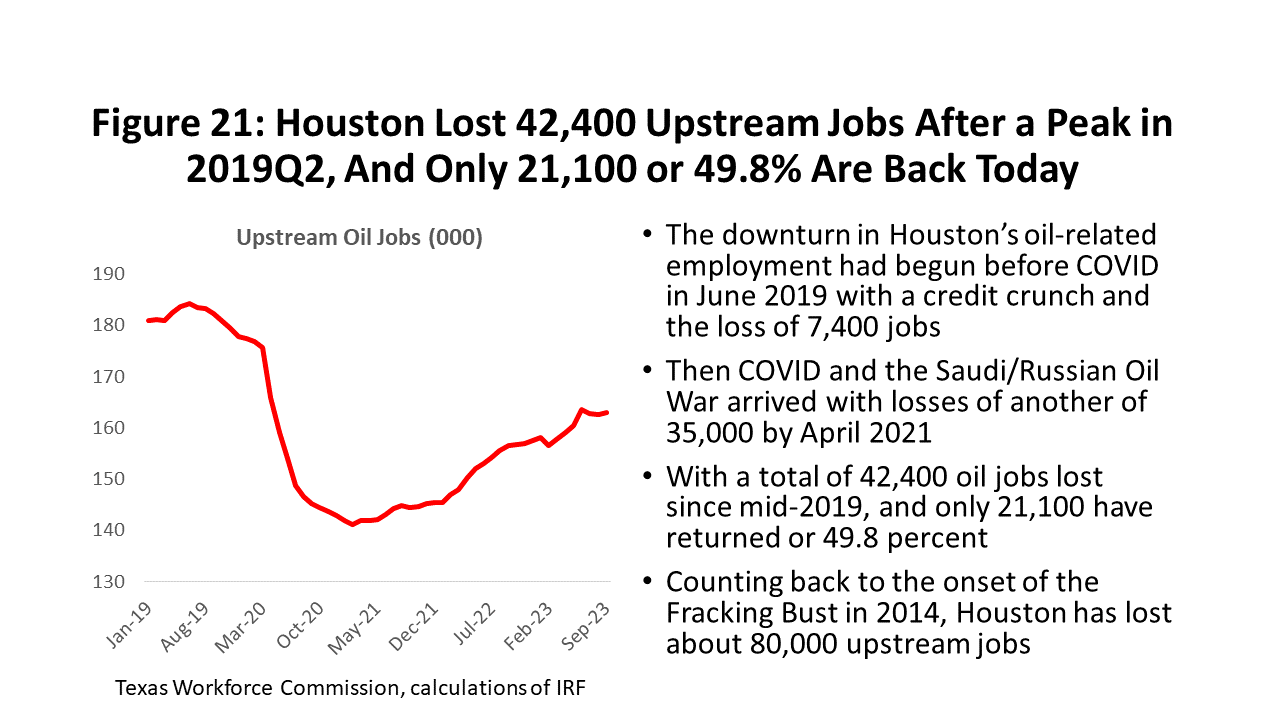

Oil-related employment in Houston has behaved much the same way as the rig count – slower and lower despite healthy oil prices. (Figure 21) After losing 42,400 upstream oil jobs to the credit crunch, COVID pandemic, and Saudi/Russian oil war, the return of these jobs continues at a slow pace. Only 21,100 oil jobs are back or 49.8 percent. If we begin counting from the end of the fracking boom in 2014, Houston has lost over nearly 80,000 jobs in oil production, services, fabricated metal, and machinery. Again, just one more sign that this is a cautious industry – smaller and slower-growing even with $70 oil.

Houston’s Employment Outlook

With COVID behind us, 2023 has seen economic fundamentals return to the driver’s seat as oil and the US economy take control. Strong signs are emerging that the policy hangover from past fiscal and monetary stimulus is disappearing. While local payroll employment best shows this hangover coming to its end, local consumer spending may join in over the course of 2023.

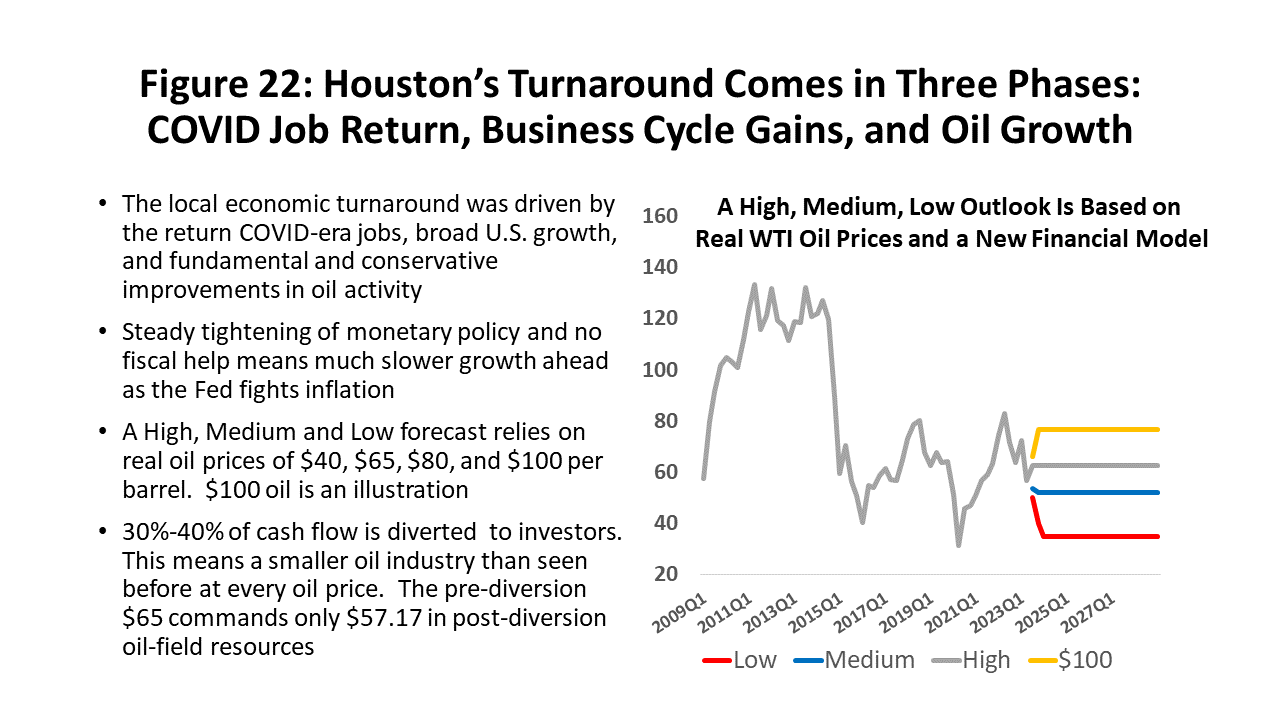

To pull the forecast together, we use a high, medium, and low outlook for planning purposes. (Figure 22) We use the price of oil as the vehicle to spread the outlook from low to high employment levels. For current planning, the low oil price is set near $40 per barrel and the high at $80. The medium price is $65 per barrel or the long-run marginal cost of oil. In all cases, we use the new financial model with 30 percent of operational cash flow diverted to investors or else used to strengthen the firm’s finances. This smaller and slower-growing oil industry reduces our expectations for oil-field expansion and now implies slower regional growth than similar prices would have implied in the past.

Oil prices currently seem likely to hold in the current $70-$80 range, but the on-going Israel-Hamas War provides for the possibility of a sharp spike up in oil price and the return of $100/b for crude, perhaps for a prolonged period of time. We have kept the high employment forecast near $80 per barrel but added the impact of a $100 oil price to demonstrate its consequences. Always a past marker for an oil-field boom, today’s $100 oil will not bring back the frenzied domestic oil-field activity of the past but can still make its mark on local job growth.

The Survey of Professional Forecasters has steadily improved its outlook for the US economy since early 2023: for 2023Q1, the forecast for job gains through the first four quarters was 32,500 jobs per month, in 20Q2 it 78,900 jobs per month, and now it is 91,000 jobs per month. This compares to pre-COVID job growth at 125,000 jobs per month. There is no US recession in the outlook -- and growth picks up quickly by the end of 2024 and moves above trend by the middle of 2025.

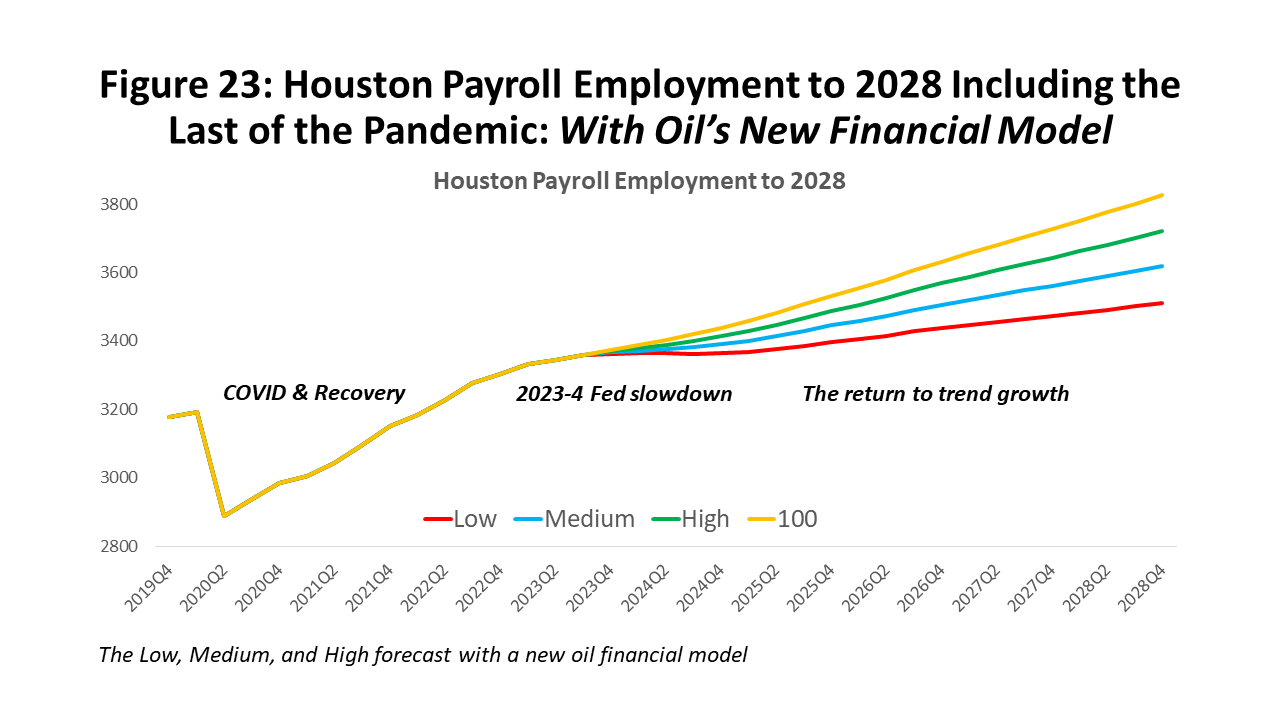

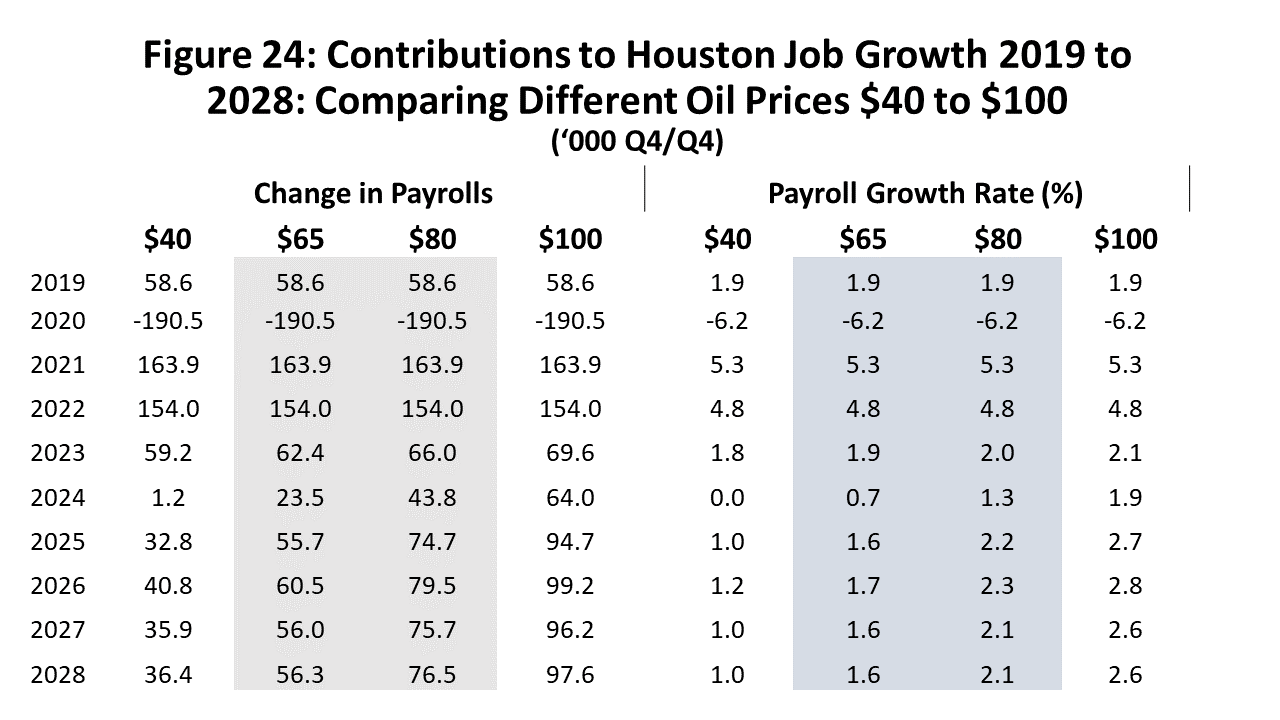

Figure 23 also shows how these economic fundamentals play out over the longer run for Houston payrolls in the low, medium, high, and $100 cases. This is our forecast of Houston’s economic future through calendar year 2028. We see the COVID lockdowns end, a long recovery to pre-pandemic employment levels and beyond, a moderate slowdown that comes in 2024 as a full year of slow growth. For Houston, growth in 2023 is a return to trend near 60,000 jobs and 2024 will average perhaps half of that. We bounce back briefly above trend in 2025 before reverting to the long-run trend.

Figure 24 is this same 2023-2028 forecast of Houston’s payroll employment stated in annual changes and measured Q4 over Q4 each year. The near-term focus of the outlook in 2024 should be between the medium and high forecasts as long as oil averages between $70 and $80 per barrel -- as it has done for the last 24 months. If oil prices continue to hold in this range, we could see around 45,000 jobs in 2024. While not a recession -- or even much of a setback -- it will feel painful after the high rates of growth that followed the pandemic.

Our outlook for oil prices in 2025 and after should be the long-term marginal cost of oil or near $65/b and US payroll employment to a trend 125,000 jobs per month. This is not because we know where they will be, but because no one knows and a reversion to the mean becomes the best default assumption. In 2025, the medium forecast shows a quick return to long-term trends at 55,700 jobs followed by with 60,500 in 2026 and 56,000 in 2027 and 2028.

Note that $100 oil would see much stronger job growth materialize at 64,000 in 2024, turning into 94,700 in 2025. Beyond that, high levels of payroll employment growth continue in the model, but any scenario would need to reimpose our “reversion-to-the-mean” rule. The Ukraine-Russia War is our most recent example of this kind of political conflict forcing a jump in oil prices, and it proved to be short-lived. And, as the old adage goes, periods of high oil prices are usually ended by high oil prices. With sufficient time, we will see conservation, new oil supplies, and slower global economic growth ultimately tame oil prices.

Written by:

Robert W. “Bill” Gilmer, Ph.D.

December 9, 2023