Houston Updates

-

Archive

- March 2025

- December 10, 2024

- September 14, 2024

- May 21, 2024

- March 19, 2024

- December 9, 2023

- June 16, 2023

- April 6, 2023

- March 17, 2023

- Dec. 19, 2022

- Sept. 14, 2022

- July 4, 2022

- March 27, 2022

- March 9, 2022

- September 2021

- April 2021

- March 2021

- September 2020

- August 2020

- June 2020

- April 2020

- March 2020

- January 2020

- December 2018

- June 2018

- March 2018

- February 2018

- January 2018

- September 2017

- September 2017 Post-Hurricane

- June 2017

- March 2017

- January 2017

- September 2016

- March 2016

- December 2015

- September 2015

- June 2015

- March 2015

- December 2014

- June 2014

- March 2014

- November 2013

- September 2013

Houston's Economic Outlook Reshaped by COVID-19 and the Oil Price War

March 22, 2020

The most compelling fact remaining from our recent forecasting efforts is our often repeated admonition that no one could predict the timing or cause of the next recession. The COVID-19 virus provides the kind of unanticipated economic shock that often triggers recession. In recent years the U.S. has seen this role filled by a financial crisis, a technology bust, and several oil-price shocks. Now another recession appears increasingly likely, but anyone who predicted this downturn surely owns a real crystal ball.

Where now? In the middle of the current uncertainty and public panic it is difficult to know where or how to begin, but a number of studies have looked at the effects of past pandemics on the economy and provide a measured starting point. The beginning is the potential losses to the labor force to illness and caretaking, as well as social distancing caused by fear of contagion. But as long as the depth and breadth of the outbreak of COVID-19 remain ill-defined, so do its economic consequences.

This report outlines some of the implications of COVID-19 for Houston’s economy. Not knowing how the disease will ultimately spread, we resort to several illustrative scenarios and their economic implications. The results are surprising compared to where we thought the economy would be just a few weeks ago, but they perhaps now look conservative compared to daily events and speculation in the press and on television.

These scenarios are about how the disease affects the economy as the virus progresses through a six-month horizon. The daily bulletins on voluntary and mandatory orders to shelter in place, the lockdown of cities and countries, closed businesses, and enforced quarantines are causing extraordinary and unpredictable short-run distortions to the economy. They are unforeseeable beyond next week. Our focus in how the economy unfolds through the rest of the year and beyond.

Adding to the angst for Houston is the recent emergence of an oil-price war between Russia and Saudi Arabia. A nice price-break for the American driver, the current low oil prices increases the likelihood of Houston seeing an economic setback. But make no mistake, the virus is in the driver’s seat, even for Houston.

The severity of the current downturn will depend on the severity of COVID-19, which is still at an early but fast-moving stage. Will it be the moderate Asian flu of 1957-58 or the harsh Spanish flu of 1918-20? And once the flu has run its course over six or more months, after all the illness subsides, economic disruptions end, and social distancing is forgotten, where will we find the economy? For both the U.S. and Houston the likely answer is that it will be in recovery from moderate recession but otherwise in stable and healthy condition.

COVID-19 and Pandemics

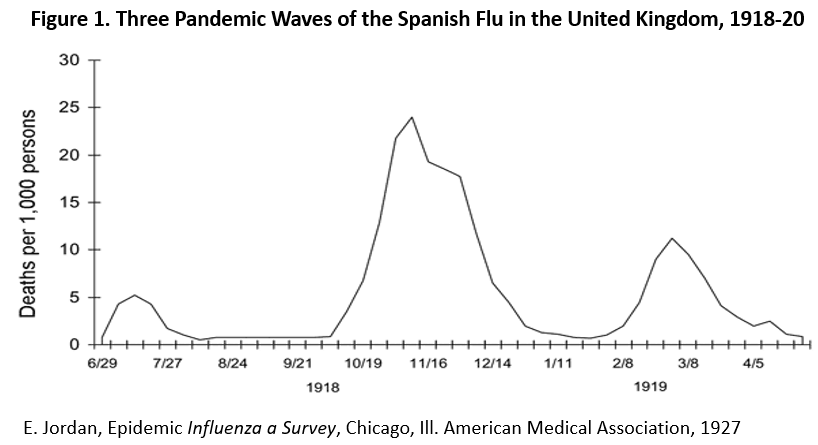

Influenza begins with a local outbreak of the disease, and the 2003 SARS virus was the first to illustrate how quickly today’s influenza can cross international borders. The number of cases reported then grows rapidly and the virus may remain widespread from three to six months, with a second wave possible one or two months later. See Figure 1.

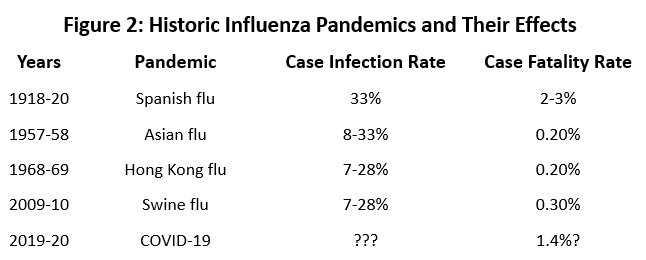

Influenza brings a sudden and urgent need for medical services as a large share of the population finds itself infected. Figure 2 shows the case inflection rate for four pandemics that have occurred since 1918. For the Asian, Hong Kong, and Swine flus we see 10-30 percent of the population infected, and 0.2 to 0.3 percent of those infected will die. The Spanish flu stands out with its 33 percent infection rate and 2-3 percent fatality rate.

The 1.4 percent fatality rate for COVID-19 has now fallen to 1.4 percent but remains a frightening statistic. We hope it is just a statement about our current ignorance about the progress of testing for COVID-19 infections.1 The reported case infection rate has been low because testing for COVID-19 was not widespread, while deaths are counted more accurately. As testing proceeds, and we find out how many people have really contracted the virus, the mortality rate could fall quickly. Some experts say it could fall to levels that would put it in a similar category as the other influenzas in Table 1.2

The number of people who contract the disease provide the beginning point for any subsequent economic analysis. There is a surge the demand for medical care, of course. But it is the disruption to the labor force through the loss of workers to illness that poses the initial threat to the economy. Those who must stay home and care for the sick add to the problem. The typical absence is about two weeks or ten workdays. With 3.2 million payroll employees in Houston, a 30 percent infection rate means nearly a million workers are infected. If we assume the virus is spread evenly over 26 weeks and lasts two weeks, we will have an average of 74,000 ill in any given week. But we know from Figure 1 that the number of cases won’t hold steady but rise from a low level to a sharp peak before falling back.

Any business could have trouble keeping enough workers to operate efficiently as the situation worsens, perhaps forcing reduced shifts or short-term closures. Then one company’s labor problems become supply chain issues for many others. Transportation links can break down due to labor shortages, or because lock-downs and shelter-in-place orders close regional or national borders and limit movement of goods and people.

Finally, a significant demand shock occurs as the fear of contagion limits social interaction. Urban areas like Houston with large numbers of densely packed people will be among the areas potentially most affected. The economic sectors most damaged by social distancing are passenger transportation, hotels and accommodation, food and drink, entertainment, retail trade, education, and some professional services.

Impact on the U.S. Economy

Houston’s economy grows from its ability to sell its goods and services (including oil) to the rest of the country. It must be able to reach outside the metro area and bring revenue from outside the region to drive local economic activity. As the saying goes, we don’t get rich by taking in each other’s laundry.

This is important now because labor force and supply chain disruptions and social distancing are reducing economic activity everywhere in the country. How far could it reduce national economic activity? How would that slowdown affect Houston?

We have three scenarios about what might happen. They encompass a broad range of economic outcomes and reflect enormous economic uncertainty about the possible outcomes for both the pandemic and the economy. This uncertainty prevails without the current short-term distortions to economic activity currently forced by the healthcare authorities.

These scenarios were suggested by a 2006 Congressional Budget Office report on the possible effects of avian flu on the economy.3 The focus is on the effects of pandemic rather than current short-term policies used to fight it.

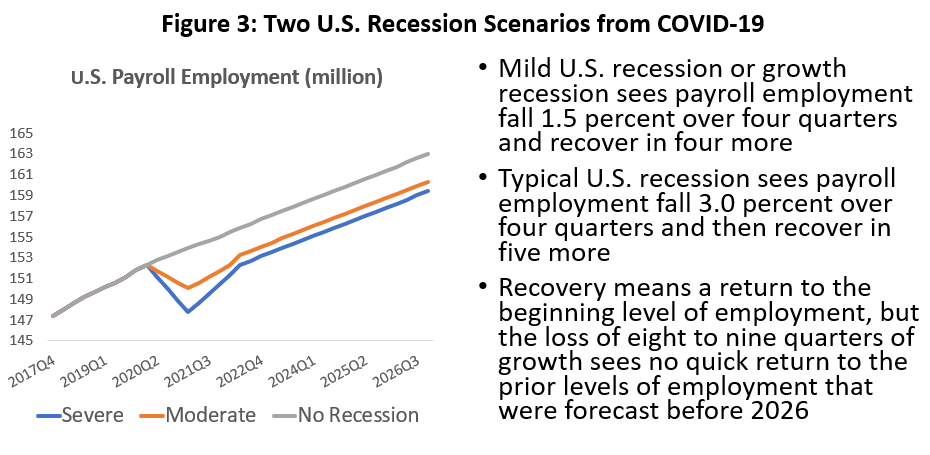

- Base Case: This is a business-as-usual scenario assuming that the viral outbreak is no worse than the seasonal flu with a 5 to 15 percent case infection rate and any macroeconomic effects are not perceptible. We use the Survey of Professional Forecasters latest report a growth projection and assume that $55 oil prices are still ahead.4 This is no longer a likely outcome, but it can still serve as a standard to measure that things have changed in just the last few weeks.

- Moderate COVID-19: This CBO model is the Asian flu of 1957-58 with a 25 percent infection rate. The CBO suggests a serious slowdown in growth or even a very mild recession would result. For our purposes, we assume a 1.5 percent fall in payroll employment over four quarters, with four more quarters needed to recover the jobs lost to recession or slowdown. The setback should be short as the economy bounces back quickly once the virus recedes.

- Severe COVID-19: The model is the Spanish flu of 1918-20 with 30 percent of the population infected and a high fatality rate. Influenza usually has a relatively low mortality rate except among the very young and old, but the high rate of death in the Spanish flu was due to the large and unusual number of fatalities in prime age groups. The CBO assumes this scenario could cause a recession typical of U.S. downturns that have taken place since 1948, or a fall in GDP of about 2.8 percent and a reduction of payroll employment of 3.0 percent. It is a four quarter decline, but with five quarters of recovery.

Figure 3 shows the effect of our assumptions on U.S. payroll employment. Both recessions share the same period of decline beginning in the first quarter, but with one additional quarter of recovery for the Severe COVID-19 case. Growth rates return to normal, but the loss of an unanticipated eight or nine quarters of normal growth leaves a considerable gap between the level of employment enjoyed before and after the recession.

Recent estimates from other forecasters such as Moody’s Analytics, Chase and Goldman Sachs have offered estimates similar to the Severe scenario in term of the depth of the decline, but which differ in terms of the timing. They assume a flat or declining first quarter, a very sharp drop in Q2, and then a bounce back in the second half of the year. Our longer recession is based partly on Figure 1, showing that as we enter the second quarter we are still near the entry-point for continued infection and mortality. Then, even as the influenza subsides or if see a second wave, many restrictions on our business and social life could remain in place if no vaccine is developed.

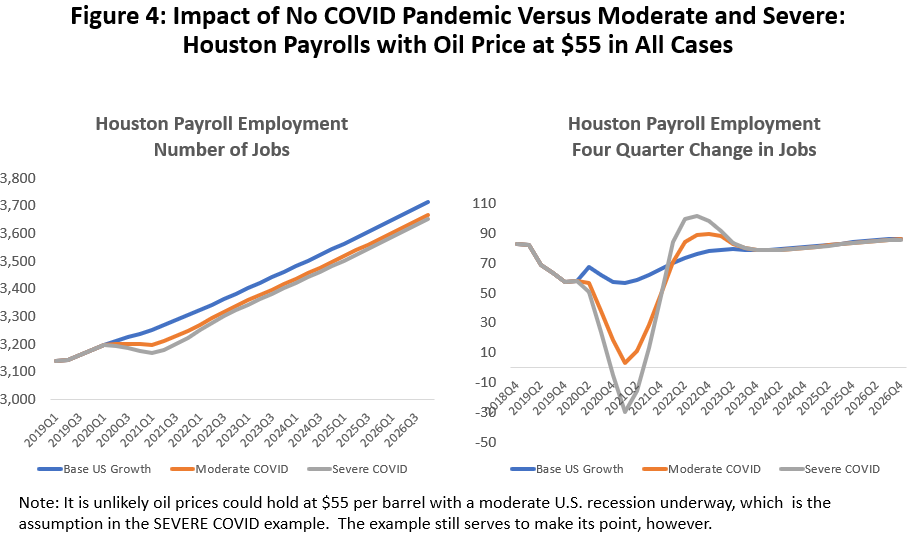

Figure 4 illustrates how Houston is affected by these hypothetical recessions. It shows the performance of Houston payroll jobs through the COVID-19 downturn and assuming that the price of oil is fixed at $55 in all three cases. We will add oil to the simulations later, but the chart tells us a familiar story about how Houston is typically less affected by economic downturns than the rest of the country. The mild downturn of 1.5 percent in the U.S. sees Houston’s job growth remain positive over four quarters, though just barely with only 8,800 net new jobs in 2020. The more serious U.S. recession translates into a Houston downturn that is half as deep as the rest of the country in percentage terms, but still results in recession and the net loss of 29,000 jobs by early 2021.5 Adding the current oil war later will worsen the outcomes.

The Oil War

Once again, Houston faces the possibility of a prolonged period of low oil prices. A dispute between Russia and Saudi Arabia over the proper price of oil has perversely turned into a fight over which country can best bear the burden of cheap oil. This sharp drop in the oil prices is a gift to the U.S. economy and a boon to the pocketbook of American drivers, but for Houston it simply adds to the economic damages already inflicted by COVID-19.

Before the arrival of COVID-19, our concern about the oil industry centered on a credit crunch. It seemed certain to lead to a shake-out of the weakest players in the fracking industry and a loss of local oil-related jobs. We had already revised the outlook for Houston down from 57,000 to 49,000 jobs for 2020 based on these credit issues.6

Looking forward, we can put most of those credit concerns to one side. They still matter, of course, but they have been replaced by a drop in oil prices that has a similar effect on producer balance sheets, except it spreads the credit crunch from the weak to everyone. The quality of the balance sheet still matters, and low prices speed up the loss of weak companies, but everyone is now facing serious cash-flow problems.

In recent years OPEC and the Saudis have learned some difficult lessons about oil prices and U.S. fracking. If they set the price much above $55 per barrel, U.S. producers quickly expanded production and stole OPEC market share. OPEC cannot set prices too low because they have national budget constraints. Even for the Saudis, a fall to $35 oil prices would create a 2020 budget deficit of perhaps 15-20 percent. The $55 range is comfortable for them.

The Russians in contrast want to repeat the oil-price experiment of 2015-16 when OPEC/Saudi withdrew as swing producer with a stated goal of damaging U.S fracking. The Russians see the Americans as now vulnerable and wants a prolonged period of oil priced at $40-$45 per barrel. Having failed badly in 2015-16, OPEC does not want to see an expensive repeat of that experiment. The Russian claim to be able to hold out for up to 10 years with oil at $25-30 per barrel, and the Saudis are calling their bluff. They already have raised exports to near 10 million barrels per day and have committed 12 million per day if needed to keep oil prices near $30.

We have three scenarios again. One is continued business as usual. Like the U.S. base forecast, it is no longer going to happen, but still serves as a marker on the extent of damage being done to the Houston economy by this turn of events. We assume oil stays at $55 per barrel going forward.

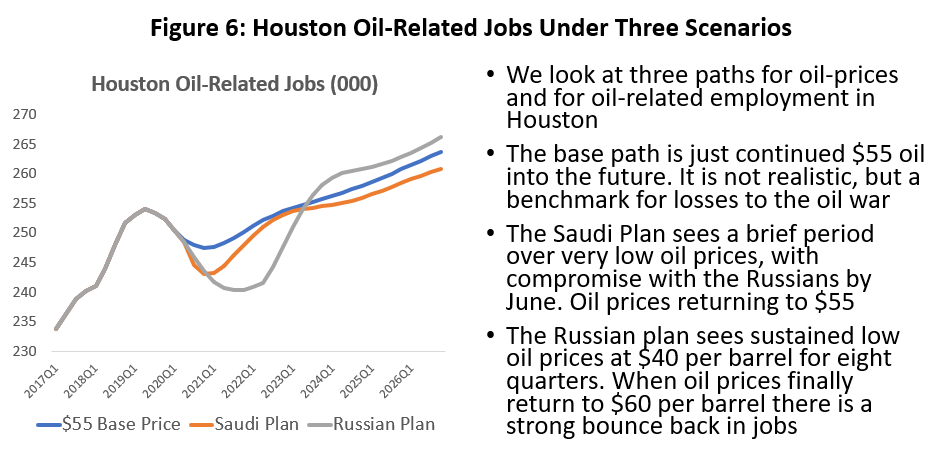

The best outcome we call the Saudi Plan, and it assumes a quick end to the dispute at the June OPEC meeting. The cost of this oil war is high for all parties, the Saudi’s seem determined to make their point, and Vladimir Putin will have looked strong on a global stage just before an April referendum that would give him another 12 years in office. The Russian Plan assumes that we get eight quarters of oil priced at $40 per barrel designed to break the back of American fracking. Oil prices then recovers to $60 per barrel.

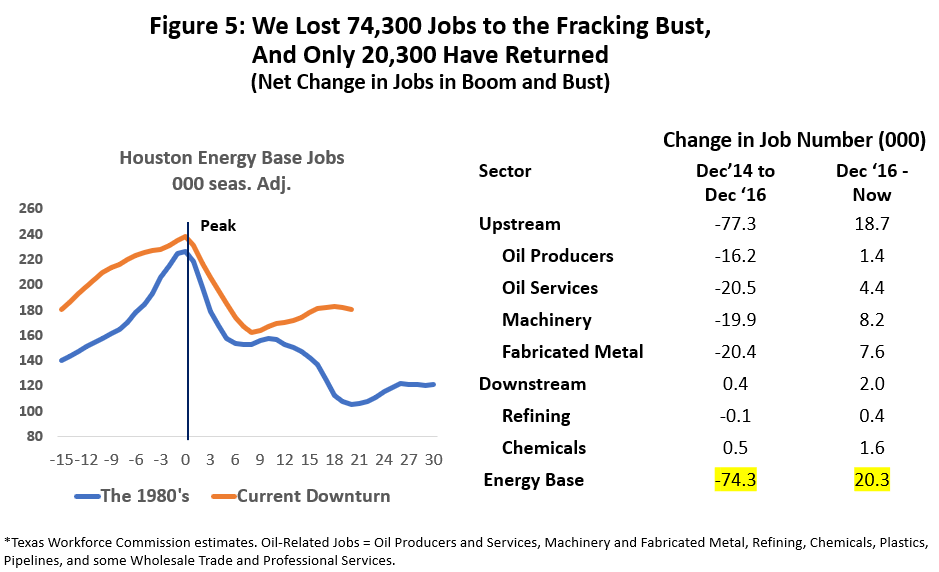

What do these low prices mean for Houston’s oil sector? Even though the objectives of the Russians sound much like a rerun of 2015-16, it will lead to very different outcomes for both American oil and Houston. Last time, an oil-price bubble burst and oil prices fell from $100 to $30 per barrel, the rig count fell from near 2000 to 404, and Houston lost 74,300 oil-related jobs. (See Figure 5.)

This time the industry is much leaner. Of the 74,300 jobs lost to the last downturn only 20,300 or 27 percent returned after 2016. Oil prices will fall from $55 to $30; the rig count had already fallen to 800 rigs because of the credit crunch; and Houston will stand to lose only 10-12,000 oil-related jobs.

Figure 6 compares the path of local oil-related employment under the three price scenarios. The Base Scenario entails only some continued oil losses in the wake of on-going credit problems. The Saudis are assumed to quickly push the oil price back up to $55 and Houston’s oil jobs quickly recover 10,600 losses. The Russian plan forces 12,600 job cuts, and is not much deeper than the Saudi Plan, but is longer lasting. The Russian Plan also brings a big positive bounce in employment after the eight quarters of low prices have passed. This assumes that the Russians were unsuccessful in crushing the American fracking industry.

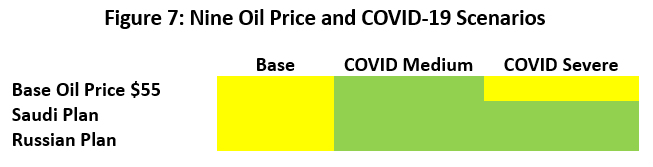

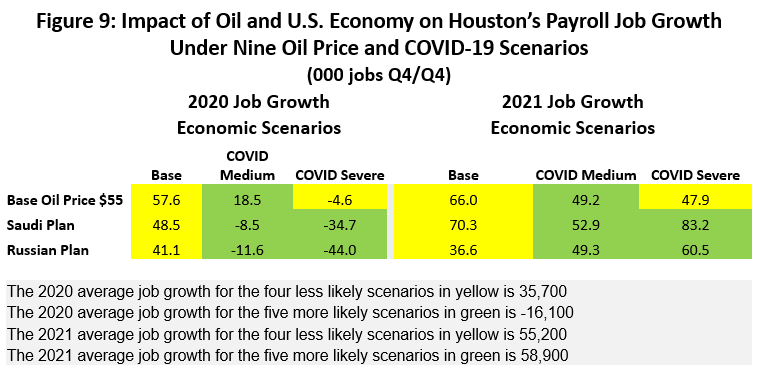

Nine Scenarios

We have nine possible outcomes: Three for COVID-19 (Base, Moderate, Severe) and three for oil prices (Base, Saudi Plan, Russian Plan). The combinations are seen in Figure 7. The yellow boxes on the left are the base scenario that no longer describes a likely future but serves simply as a marker for how far our outlook has fallen. The other yellow box is an unlikely combination of a typical U.S. recession and sustained oil prices at $55. A U.S. or global recession typically pulls oil prices down as the demand for oil shrinks. The five green boxes are alternative descriptions of how the oil price war and COVID-19 might affect the Houston metro area.

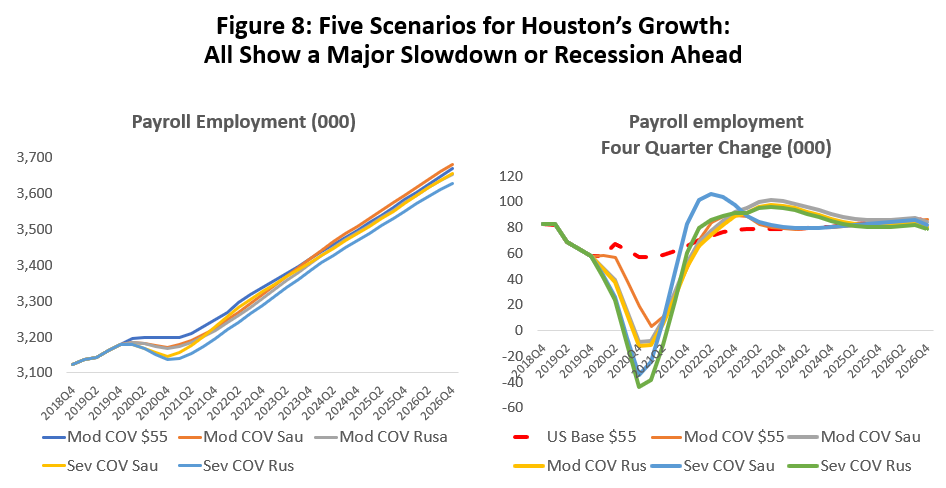

The five working combinations for Houston are shown in Figure 8, with total payroll employment on the left and four quarter changes in jobs on the right. The broken red line at the top of the righthand chart shows the steady job growth at 60,000 net new jobs, just as expected with no virus and $55 oil. The remaining alternatives do not work out well for Houston. They range from few or no jobs in 2020 to slipping into recession with a loss of over 40,000 jobs.

The COVID-19 recessions both find a trough in the fourth quarter of this year. The Saudi Plan returns oil to normal by mid-year, and the only lingering problem would be the Russian Plan still at work into early 2022. The general business-cycle rule is the steeper the fall into recession, the faster the economy bounces back. The principle is clearly at work in Table 7. After the recovery is complete, we return to normal long-term growth rates.

Figure 9 shows the estimated net change in Houston’s payroll employment for 2020 and 2021 for all nine scenarios. The fourth quarter marks the trough of the recession, and improvement begins in early 2022 in all cases. Across the bottom of the chart we see the job growth we previously expected and have been forced to discard as less likely (sum of the yellow boxes) versus the five green boxes that remain realistic. For 2020, the yellow boxes are a measure of what was lost versus the unexpected losses in green. For 2022, all the boxes return to growth as the virus and its economic damages come to an end.

Illness, Caretaking, Supply Disruptions, and Social Distancing

We have accounted for how COVID-19 virus affects the rest of the U.S. economy and how that in turn affects Houston. Houston relies on sales outside the region to grow, and falling activity throughout the rest of the country has brought the slowdown or reversal described above.

However, there are specific disruptions to the local area that won’t get counted from events happening elsewhere. Local illnesses will add to the loss of jobs; local labor shortages and supply chain issues force temporary layoffs; social distancing and mandatory health regulations threaten jobs. The extent of these losses will remain unknown across the metro area for six months or more.

For Houston, these specific local problems are in addition to losses driven by a slower U.S. economy. These large and sudden changes in local employment mean that the nice smooth curves in Figure 8 will be look much bumpier, reflecting a wild ride in front of us in 2020.

Let’s first consider worker losses to illness and figure out how many workers come and go each month due to COVID-19. Our scenarios above were driven by payroll employment, so we want to measure the number of payroll workers that might lose their jobs to a virus.

Payroll workers are about 74% of total employment in Houston with contractors and the self-employed making up the rest. Payrolls are a count of the number of workers eligible for unemployment compensation. The fall in these numbers in the face of widespread disruptions is often surprisingly small. For example, major hurricanes bring preliminary evacuations, everyone must shelter in place, and there is a period of recovery as roads are cleared, electricity restored, and the ship channel reopened.

After accounting for normal economic activity in the economy, the number of payroll jobs lost to Hurricane Ike was 22,800, 15,000 for Harvey, and 7,300 for Alicia. Houston was half its current size when Alicia hit in 1983. This is a case where every business must close, and everyone shelters in place, yet the numbers are surprisingly low. This is partly because about 76 percent of U.S. workers have some form of sick or annual leave and stay on the payroll. Others can work from home even if not covered, and employers are often willing to make accommodations to avoid dropping good workers from payrolls in difficult times.

For Houston’s 3.2 million workers, suppose 25 percent (825,000) contract COVID-19 and are out of work two weeks. The virus is active for 26 weeks, infecting on average 39,600 employees each week. We then have twice that number -- new cases plus the week before – who are out sick on average throughout the crisis. Add another 25 percent to the number of sick workers to account for care-taking. With 24 percent of employees having no leave, an average of 19,000 are off the payroll through 2020Q2 and Q3.

Based on our hurricane comparison, 19,000 is probably a significant exaggeration, but let’s say they the numbers are right. Average annual employment for 2020 would fall by 9,500 jobs compared to the year before because of the illness. The smooth path of employment growth or decline in 2020 suddenly has a couple of big bumps along the road.

Similar bumps will appear with six months of labor force shortages, supply chain issues, and social distancing and mandatory restriction. These month-to-month losses are likely to be very large indeed through the second and third quarter of this year, and with luck will tail off substantially in the fourth. The pattern of those losses is simply unknown.

A recent estimate from Wells Fargo’s economic group is that U.S. losses from this past month alone has cost perhaps 25 percent of monthly GDP or $450 billion.7 They point out that it is a less frightening number once you know that Congress is considering a $2.0 trillion aid package. The problem will be pairing up the federal money with the businesses and individuals actually hurt by the virus.

COVID-19 restrictions on our activities have been less in Texas than other states. Schools, bars and gyms are closed; restaurants are restricted to delivery and take-out only; gatherings are limited to ten people or fewer; employees are encouraged to work from home where possible. Combine this with corporate and public sector restrictions on travel, social distancing, and falling employment needs, and a good part of Houston’s payrolls are at risk.

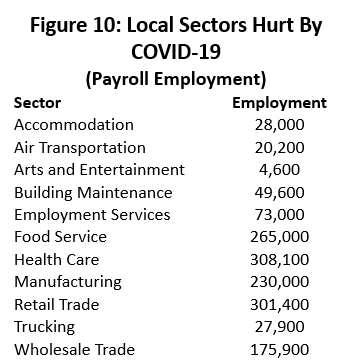

Sectors most at risk are listed them in Figure 10. Health care is the only positive. Accommodation and air transportation are hurt by travel restrictions. Arts and entertainment get combined with the large retail and food service sectors as targets of social distancing. Food is additionally damaged hurt by service restrictions. Building services shrink with empty schools and offices. Employment services shrink along with the economy and general uncertainty.

Goods sectors are caught up in labor shortages and supply chain problems. Trucking and trade slow in their wake.

Some sectors are already hurt, and others will follow an unpredictable path carve out by COVID-19 and healthcare authorities. Altogether 1.5 million workers or 47.5 percent are at risk to some degree. We have no way to know what changes will occur in the next few months.

Summary and Conclusions

Our story is one of moderate recession in Houston that will feel much worse as we pass through it. With the health officials directing efforts to protect the community, we will see large, unpredictable short-term swings in employment, levels and general business activity. We estimate Houston’s economy could be on a steady path to lose as many as 44,000 jobs by year-end 2020, with the figures potentially looking much worse through the second and third quarters of the year.

As the virus progresses, the loss of workers and caretakers to illness would subtract a steady 10-20,000 workers from payrolls. Then labor force shortages, social distancing, supply disruptions, and public health policy will simply pile on an unknown number of additional job cuts. These losses come on top of the effects of a national recession that would be underway.

Then as the virus recedes, all of this turns around. There are no more workers out sick, and fear of the virus and its spread will end. If no vaccine is developed there could be a residual need for some intervention by authorities into 2021, but most economic damage could be reversed by year-end. We would be left in Q4 with the residual effects of a national and local recession and the possible loss of 44,000 jobs in Houston, but with a quick recovery to come in 2021.

When economists look back at Houston’s long-term growth, the first thing we do is remove the extraordinary one-time events that distort the history of the underlying business cycle, like hurricanes, Y2K, Super Bowls, or COVID-19. This is to remove the temporary distortions and find perspective on the basics of the economy through time. This is also what Figures 8 and 9 are telling us about what is to come through the middle of this year: Ignore the one-time bumps to see the big picture.

A reminder that these are scenarios or made up events for illustration. We started them with the premise that all the economic effects of COVID-19 begin with the behavior of the virus and how it will affect the public, and that remains a mystery as this is written.

That COVID-19 will pass after six months does not make the personal and business damages from the virus any less. They are frightening today because there are large unknown economic consequences to come. When we look back, if you were ill, lost your job, or your business suffered a setback, it will always be remembered as a terrible time. But once the pandemic and its losses end, Houston moves on from a moderate recession to renewed growth.

Written by:

Robert W. Gilmer, Ph.D.

Institute for Regional Forecasting

March 22, 2020

Notes

1The U.S. mortality rate was 3.7 percent on March 15 according to the World Health Organization, Current Situation Report 55. Recent introduction of widespread testing has brought the numbers down to 1.3 percent in just a week.

2“Why Are COVID-19 Death rates So Hard to Calculate? Experts Weigh In,” Medical News Today, March 5, 2020

3Congressional Budget Office, A Potential Influenza Epidemic: Possible Macroeconomic Effects and Policy Issues, revised report July 22, 2006. https://www.cbo.gov/sites/default/files/109th-congress-2005-2006/reports/12-08-birdflu.pdf; also see Jon-Wha Lee and Warwick J. McKibbin, “Globalization and Disease: The Case of SARS,” Brookings Discussion Papers on International Economics, No. 156, February 2004 and Alexandra A. Sidorenko and Warwick J. McKibbin, “A Potential Influenza Epidemic: Possible Macroeconomic Effects and Policy Issues,” Centre for Applied macroeconomic Analysis, Australian National University, February 2006.

4Federal Reserve Bank of Philadelphia, Survey of Professional Forecasters, February 14, 2020.

5The picture is not as sanguine once lower oil prices are added, and the current OPEC/Russia dispute aside, the price of oil almost always falls with a national or global recession. Houston typically gets a double-blow from the national downturn and the price of oil Despite this, even counting the oil price fall, Houston’s recessions are typically milder. We grow faster than elsewhere anyway, drawing on lower home prices, lower taxes, and less regulation.

6The reference in note 1 contains a long discussion on the oil-industry’s recent credit problems.

7Wells Fargo Economic Group, How Can We Quantify the Potential Loss in U.S. Income? March 19,2020